Go Dawgs!

Ticor has gone purple in support of our UW Huskies! Win or lose in the Bowl Championship Series, it has been a great season for the local boys!

Ticor has gone purple in support of our UW Huskies! Win or lose in the Bowl Championship Series, it has been a great season for the local boys!

You’re a real estate agent, so you know that buying a home can be overwhelming for many of your clients. Homebuyers can easily feel confused and frustrated by the mounds of paperwork they have to sign. Plus, all the fees associated with closing can sometimes be a surprise even to an experienced buyer.

Owner’s title insurance is one of those items often misunderstood by homebuyers at closing, yet its value is tremendous. As an important advisor to your clients, you are in the position to help them understand the value of owner’s title insurance and the dangers that can be incurred without it.

Owner’s title insurance is a policy that protects homebuyers’ property rights. For the same reasons that the bank requires a lender’s insurance policy, a homebuyer obtains owner’s title insurance to protect their legal claims to the property.

What is a title commitment

What to look for in a title insurance company

The Benefits of an owner’s title insurance policy

Say, for example, your client recently purchased a new home from a builder, but the builder failed to pay the roofer. Wanting to be paid, the roofer filed a lien against the property. Without owner’s title insurance, your client would be responsible for paying this existing debt—meaning they’d be paying the roofer out of pocket instead of purchasing something nice for their new home, like new living room furniture. This is just one example of how owner’s title insurance protects homebuyers’ from various significant risks. With owner’s title insurance, your client would be protected from certain legal or financial responsibilities.

The good news is that owner’s title insurance protects homebuyers financially, as long as they or their heirs* own the home. For a low, one-time fee (average of 0.5% of purchase price), homebuyers can rest assured, knowing they are protected from inheriting existing debts or claims to their property.

Each state government regulates its own title insurance costs. In addition, the Consumer Financial Protection Bureau (CFPB) regulates closing and settlement practices which can impact title insurance. Keep in mind that title insurance industry practices vary due to differences in state laws and local real estate customs. The party that pays for the owner’s title insurance policy varies from state to state, and sometimes even within a state. For more information about title insurance, or to find a company approved to issue an owner’s policy, please direct your homebuyer clients to www.homeclosing101.org.

Together, real estate agents, land title insurance professionals and other stakeholders involved in real estate transactions can protect homebuyers and provide them with the peace of mind they deserve during the home closing process.

For more information about title insurance, and to get free resources for real estate agents, visit www.alta.org/realtor.

*This article offers a brief description of insurance coverages, products and services and is meant for informational purposes only. Actual coverages may vary by state, company or locality. You may not be eligible for all of the insurance products, coverages or services described in this advertising. For exact terms, conditions, exclusions, and limitations, please contact a Ticor Title representative.

To celebrate the season, have some fun, and ultimately provide support for those in need, members of the Ticor Title family took to the streets of Redmond for the merriest 5k of the year on December 3rd – The Ugly Sweater Run.

Needless to say, we donned our craziest sweaters, had a blast, burned a few calories, and feel proud to have contributed to a cause that brings warmth to our community.

The Ugly Sweater Run is partnered with One Warm Coat, an organization that provides a warm coat, free of charge, to anyone in need. Participants of the run are also encouraged to bring a warm coat for donation. In the past year, One Warm Coat held 3,544 coat drives, collected 586,117 coats, and had an impact of $16,680,269.

Ticor Title is happy to offer the House Hunter Scorecard, a simple tool designed to improve the home-buying experience.

Deciding on which home to purchase is a major commitment that involves evaluating location, size, price, amenities, and so many other factors. With so many characteristics to assess and compare, it helps to have a tool that can itemize factors, clarify expectations, and build confidence that the home-buyer’s ultimate home choice is the best fit for their desired lifestyle.

After weeks of looking, it may be easy for a buyer to forget what exactly they liked about homes they’ve viewed. Over time, the details may fade or become vague. However, the House Hunter Scorecard helps to keep a record by organizing and comparing what the buyer likes best about their top two or three home choices.

The House Hunter Scorecard not only includes most of the features needed in a home, it takes into account the importance of the surrounding community and helps the buyer to visualize the lifestyle they seek.

With the House Hunter Scorecard you can set up a priority list ahead of time and a rank & order features from the most vital to insignificant. This helps to bring focus to the decision making process. Since most home purchases involve compromises on preference, the scorecard helps to weigh the options and make home comparisons easier.

The priority list can also help a Real Estate Professional get a better picture of what the buyer is looking for in a house so they can more accurately suggest houses available that best meet the requirements.

When visiting different homes, buyers can leverage this check list to make notes, see the big picture, and build confidence that their ultimate choice is the best fit for their needs and vision.

We are pleased to announce that the Ticor Title Spokane Valley office will have a new location as of Friday, November 18 in the RiverView Corporate Center. Our new location will provide improved amenities, greater accessibility, and a more upscale experience for our Spokane Valley clients and partners. You can expect the same high standards of service from our current Spokane Valley team of professionals.

16201 E Indiana Avenue, Suite 3300

Spokane Valley, WA 99216

(509) 928-9665

At Ticor Title we believe that every successful closing begins with a great team. We understand what it takes to provide superior service to our clients and partners in the timeliest manner. Our team of professionals go above and beyond to create a better closing experience by offering same-day signing/closing and instant delivery of Closing Protection Letters.

Click the following link to download a printable version of – Same-Day Solutions – CPL, Sign, Close .

Click the following link to download a printable version of – Same-Day Solutions – CPL, Sign, Close .

Because of our commitment to higher standards of service and the high degree of skill and efficiency of our escrow staff, Ticor Title offers same-day signing and funding on purchase and refinance transactions. We have the ability to work closely with our lending partners in order to provide escrow signing services, document delivery to the lender, and recording/closing in the same day. The result is that the buyer has a better experience at the end of the transaction and can get into their house sooner!

Our lender clients may request Closing Protection Letters on active transactions with Ticor.

We offer the most efficient approach to providing our lending partners with Closing Protection Letters. With our electronic CPL request form, we have the ability to fulfill the request and update the escrow file in one minute. With 24/7 availability and instant response, we fulfill the lender requirement and eliminate a potential roadblock to closing so the transaction can progress.

Ticor Title is the company that can and will do what it takes to provide the higher standards required for the best possible closing experience. With our rich Pacific Northwest history, unmatched financial strength, and client-focused leadership, it’s clear that Ticor Title is the right choice!

Buying a home is an exciting and emotional time for many people. To help you buy your home with more confidence, make sure you get owner’s title insurance. Here’s why it’s so important for you.

Buying a home is an exciting and emotional time for many people. To help you buy your home with more confidence, make sure you get owner’s title insurance. Here’s why it’s so important for you.

Unforeseeable title claims, such as:

● Forgery: making a false document. For example, the seller misrepresents the identity of the person selling the property.

● Fraud: deception to achieve unfair gain. For example, someone steals your identity and either sells your house without your knowledge or consent, or takes out a second mortgage on the property and walks away with the money.

● Clerical error: inconsistent paperwork and historical records. For example, an unforeseeable discrepancy in the property or fence line causes confusion in ownership rights.

Unexpected title claims, such as:

● Outstanding mortgages and judgments, or liens against the property because the seller didn’t pay required taxes

● Pending legal action against the property that could affect your ownership

● An unknown heir of a previous owner who is claiming ownership of the property

Click here to download 7 Reasons Why Every Home Buyer Needs Owner’s Title Insurance.

Click here to download 7 Reasons Why Every Home Buyer Needs Owner’s Title Insurance.

More Homebuyer Tips & Information

The American Land Title Association helps educate homebuyers like you about title insurance so you can protect your property rights. Check out www.homeclosing101.org to learn more about title insurance and the home closing process.

*This article offers a brief description of insurance coverages, products and services and is meant for informational purposes only. Actual coverages may vary by state, company or locality. You may not be eligible for all of the insurance products, coverages or services described in this advertising. For exact terms, conditions, exclusions, and limitations, please contact a Ticor Title representative.

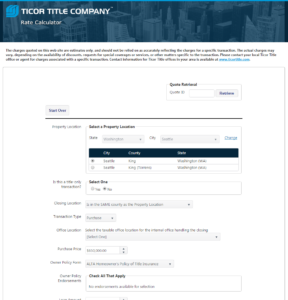

Sometimes it’s the little things that can make all the difference as to how smoothly a real estate transaction flows. Among the little things are Title & Escrow Rates and Closing Protection Letters (CPLs). The old school way of receiving accurate title & escrow rates or a CPL involved contacting an escrow officer or assistant to request information specific to a transaction. But what do you do if it’s after hours or on the weekend? What if your preferred closer is unavailable or in a signing appointment? What if your deal may fall apart if you don’t receive an answer immediately?

Click to view TicorRates.com Title & Escrow Calculator

Visit TicorRates.com for instant rates.

In addition, for transactions in which an owner’s policy will be purchased, the CFPB rule prescribes special mathematical calculations for disclosure of the owner’s and lender’s title insurance premiums, which may require receipt of rates for both a stand-alone and simultaneously-issued lender’s policy, as well as the owner’s policy rate. Suddenly, the little task of getting a quote has become a high-stakes math project.

The Ticor Title rate calculator takes all the aforementioned variables into account and provides a means of accessing accurate fees instantly any time, any day. The result is streamlined workflows for our clients and the peace of mind and confidence that comes with accurate numbers.

The CFPB has amended Regulations J and L to permit online filing under ILSA. According to the CFPB, “the Interstate Land Sales Full Disclosure Act requires certain land developers to register their subdivisions and provide disclosures about the lots being offered, to protect consumers from deception or abuse.” This generally requires a developer of a subdivision containing one hundred or more lots, with certain exceptions, to register the subdivision with the CFPB. Electronic filing will modernize the process by making payment submission more efficient and reducing paperwork costs.

For issues or questions regarding ILSA registration contact the Interstate Land Sales Registration Program Office. Direct any FOIA requests to our FOIA office.

CFPB_ILSAProgramOffice@consumerfinance.gov

(202) 435-7800

The agency has also launched a new website with online filing resources, including instructions, available at

www.consumerfinance.gov/ilsa.

June 10, 2016

When people talk about a real estate purchase, they sometimes use the terms “signing” and “closing” interchangeably in reference to the event when the buyers sign documents with Escrow. However, there are several events that take place between the buyer’s signing appointment and the actual closing of the real estate transaction. Let’s take a moment and review that process.

Escrow receives instructions to prepare the settlement statement so the lender can provide the Closing Disclosure to the buyer/borrower for acceptance and signature. During the waiting period, the escrow company can prepare the necessary escrow and title transfer documents. After the required waiting period, the lender will then forward the documents for signature to the escrow company, so that the signing appointments can be scheduled.

Once the loan documents have been signed, the escrow officer delivers them back to the lender either by email, fax or physical delivery for review. When the lender is satisfied that all required documents have been signed and all outstanding loan conditions have been met, the lender will notify escrow that they are ready to disburse the loan funds to escrow. Upon receipt of the wire from the lender, the escrow officer is authorized to send the transfer documents to the county for recording. The time frame for review is normally 24 to 48 hours.

Download a printable version of this article. CLick the following link: What Happens Between Signing and Closing of Escrow

Real estate transactions in Washington State that involve conveyance or transfer where consideration is paid, require the payment of excise tax. All appropriate tax amounts must be paid before the county will allow the Deed conveying title to be recorded.

Once recording is authorized by the lender, and all funds have been received, documents are either electronically recorded or hand-carried to the county recorder’s office by the title insurance company. The Warranty Deed is recorded first, showing the transfer of the property to the buyer, with the Deed of Trust recorded next. Recording the Deed of Trust just after the Deed insures the lender’s first lien position on the property.

Recording numbers are the unique and specific numbers given by the county recorder’s office to a properly executed legal document thereby making it part of the public record. In other words, when we have recording numbers, the buyer is “on record” as holding title to the property and based on the possession date in the purchase agreement, the new owner may take possession and proceeds may be disbursed to the seller.

![]()