Remember to set your clocks forward this weekend!

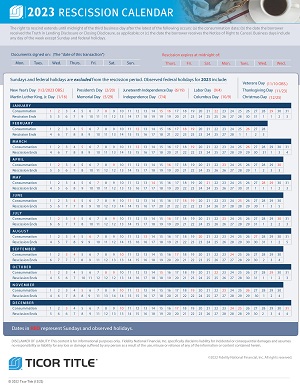

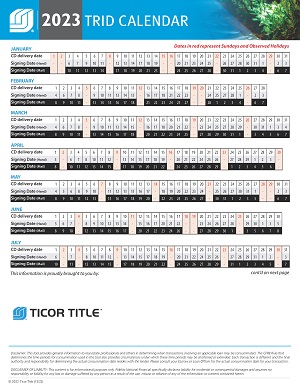

As we begin 2023, our annual County Recorders’ Office Holiday Calendar, TRID Calendar and Rescission Calendar are now available for download.

Happy Presidents’ Day from Ticor Title!

Our office will be closed on Monday February 20th, 2023 in observance of the Holiday. Thank you!

Please join us in celebrating Black History Month throughout the month of February.

Did you know that Ticor Title is focused on cultivating new investor friendly opportunities in this current market?

This Seattle area report includes a detailed list filled with information for you to review and consider when talking to your clients about investing in Seattle Real Estate. Ticor Title is committed to being Seattle’s Investor Friendly Title Company for 2023!

For a monthly fee of 20.00, you will receive a detailed list providing pre-foreclosing lien information along with all of the properties that went into foreclosure recently.

The list will include…

• List covers King, Pierce, Snohomish and Kitsap Counties.

• Contains both trustee sale and judicial foreclosure filings.

• Sent each Friday afternoon.

Detailed Pricing – Cost is $20/month, or $200/year. $200 buys 52 weeks of the 4-county list; a really good value. *Paying annually ensures uninterrupted service.

Contact your Sales Executive today to find out why Ticor Title is Seattle’s Investor Friendly Title Company!

We would like to invite you to attend this specially crafted class series all about Creative Closings in our current market.

Click here to RSVP, seating is limited! https://tinyurl.com/yck7344r

We’ll Cover

| MORTGAGE ASSUMPTIONS – An assumable mortgage is a loan that can be transferred from one party to another with the initial loan terms remaining in place. CONTRACT ASSIGNMENTS – A contract assignment allows a buyer/investor to assign their interest in a Real Estate Purchase and Sale Agreement to a third party (normally for a fee). WRAP TRANSACTIONS – A Wrap is a type of seller financing wherein the seller’s existing loan is wrapped by a secondary loan from buyer to seller. The payment from the buyer is then used to pay the sellers existing loan. SELLER FINANCING – Real estate contracts vs notes / deeds of trust |

Our office will be closed on Monday January 2nd, 2023 in observance of the Holiday. Thank you!

We would like to invite you to attend this specially crafted class series all about Creative Closings in our current market.

Click here to RSVP, seating is limited! https://tinyurl.com/yck7344r

We’ll Cover

| MORTGAGE ASSUMPTIONS – An assumable mortgage is a loan that can be transferred from one party to another with the initial loan terms remaining in place. CONTRACT ASSIGNMENTS – A contract assignment allows a buyer/investor to assign their interest in a Real Estate Purchase and Sale Agreement to a third party (normally for a fee). WRAP TRANSACTIONS – A Wrap is a type of seller financing wherein the seller’s existing loan is wrapped by a secondary loan from buyer to seller. The payment from the buyer is then used to pay the sellers existing loan. SELLER FINANCING – Real estate contracts vs notes / deeds of trust |

Happy Holidays from Ticor Title! Our office will be closed on Monday December 26th, 2022 in observance of the Holiday. Thank you!

![]()