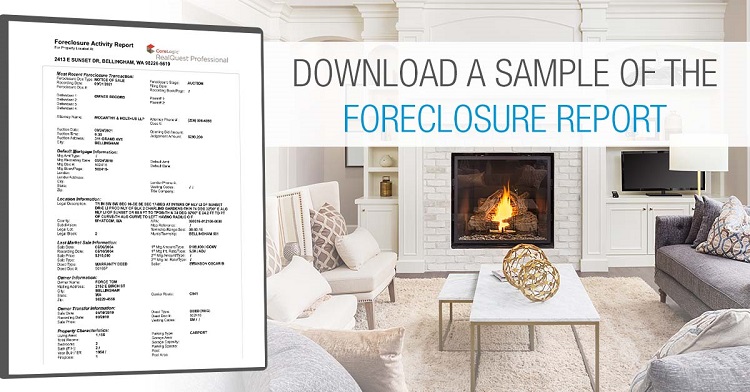

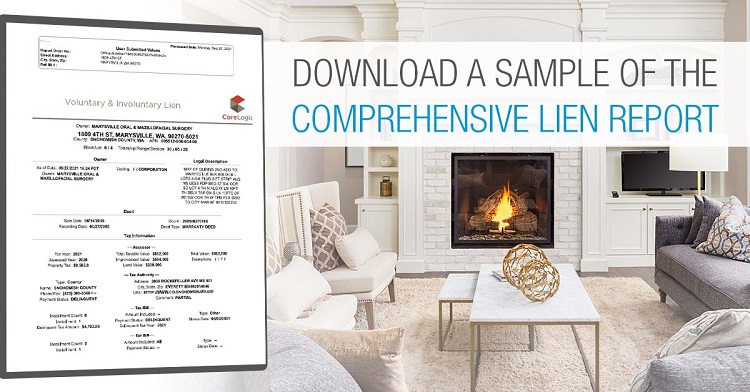

Download a sample of the Comprehensive Lien Report

Analyze your subject property’s lien position and quickly understand its financial situation

• Deeds of Trust of record • Mortgage Modifications and assignments • Releases • Notice of Trustee Sale – Foreclosure filings • Judgments • Bankruptcy • Personal Tax Liens • HOA/Mechanics Liens • Property Tax Status

Significantly reduce cost – less than a full title report or lender equity report. Saving you time – most reports are available the same day.

There are few things in life that are as certain as taxes, especially when it comes to buying, selling, and owning real estate. In this article, we examine property taxes in Washington State, including when they are due, when they may be paid, how they’re calculated, and what tax relief programs are available.

Here’s an excerpt from ID Affidavit – Why Is It Needed? in our guide:

An ID Affidavit provides title companies with the information they need to distinguish the buyers and sellers of real property from others with similar names. After identifying the true buyers and sellers, title companies may disregard the judgments, liens or other matters on the public records under similar names…

We would love to help you have an amazing closing experience on your next real estate transaction.

A Title Commitment (also known as a Preliminary Report in some areas) is a dated formal report that sets out in detail the conditions under which a policy of title insurance would be issued on a particular parcel of land. Its sole purpose is to facilitate the issuance of the policy.

Here’s an excerpt from What is the Title Commitment in our guide:

A Title Commitment provides a list of the matters which will be shown as exceptions to coverage in a designated policy or policies of title insurance, if issued concurrently, covering a particular state or interest in land. It is designated to provide a preliminary response to an application for title insurance and is intended to facilitate the issuance of the designated policy or policies. It is normally prepared after application (order) for such policy(ies) of title insurance on behalf of the principals to a real property transaction.

We would love to help you have an amazing closing experience on your next real estate transaction.

A “red flag” is a signal to pay attention! Below are some of the items which may cause delays or other problems within a transaction and must be addressed well before the closing.

The questions, “What is an Escrow?” or “Why do I need Escrow?” come up from time to time. To answer these common questions and more, we have assembled an easy-to-understand Buyer and Seller Guide to Title and Escrowfor our clients and partners.

Here’s an excerpt from Escrow: Frequently Asked Questions in our guide:

Why is Escrow Needed? Whether you are the buyer or the seller, you want assurance that no funds or property will change hands until all instructions have been followed. With the increasing complexity of business, law and tax structures, it takes a trained professional to supervise the transaction.

How Long is an Escrow? The length of an escrow is determined by the terms of the purchase agreement/joint escrow instructions and can range from a few days to several months.

Who Chooses the Escrow? The selection of the escrow holder is normally done by agreement between the principals. If a real estate agent is involved, they may recommend an escrow holder.

We would love to help you have an amazing closing experience on your next real estate transaction.

We are often asked, “Why do I need title insurance?”, and “What does title insurance protect?”. To answer these common questions and more, we have assembled an easy-to-understand Buyer and Seller Guide to Title and Escrowfor our clients and partners.

Here’s an excerpt from The Title Insurance Value Proposition in our guide:

Title insurance protects the interests of property owners and lenders against legitimate or false title claims by owners or lien holders. It insures the title to the investment, unlocking its potential as a financial asset for the owner.

Title problems are discovered in more than one-third of residential real estate transactions. These “defects” must be resolved prior to closing. The most common problems are existing liens, unpaid mortgages, and recording errors of names, addresses or legal descriptions.

A homeowner’s title insurance policy protects the owner for as long as he or she has an interest in the property; and the premium is paid only once, at closing.

We would love to help you have an amazing closing experience on your next real estate transaction.

At Ticor we strive to create a unique and personal closing experience that is unmatched in the industry. As many of our clients know, our closings are smooth and consistent time after time.

These are just a few of the reasons why working with Ticor is like being at your favorite coffee house!

The Ticor Difference:

We take a proactive approach from beginning to end.

Files are opened immediately.

Title is cleared and all items needed for closing are obtained within ten days of opening. This means no surprises at closing for items missed or simply not addressed.

We sign our sellers in advance to ensure they sign at a date, time and place that is convenient for them.

We can better accommodate same day buyer signings and closings because our sellers are already signed.

We send file updates throughout the transaction to keep our clients in the loop of what comes next.

We e-record all of our documents which allows us to get the recording numbers back to our clients ASAP.

We use the customer preferred method of communication by phone calls and texting which makes it easy and convenient for our agents and clients to communicate with our team.

Since our closers work in teams there is always someone available to speak with or answer questions for clients.

We invite you to stop by one of our ten beautiful offices – coffee is on us!

In March of 2018, Governor Inslee signed the Washington Uniform Common Interest Ownership Act (WUCIOA) and it took effect on July 1, 2018. The bill created a new chapter in the Revised Code of Washington that governs the formation, management, and termination of condos, co-ops, and planned communities (Common Interest Communities or “CICs”). Below is a summary of the who, what, when, where, and why of the act.

Who does the act apply to?

All new common interest communities meeting minimum requirements, or existing communities who “opt in” by amending existing CCRs.

Applies to the Formation, Management and Termination of “Common Interest Communities” (CIC)

Affects how new CICs are created in Declaration of CCRs and Map

Existing HOAs and Condos may Opt-In by Amendment

Affects new Construction Sale of Units by requirement of Public Offering Statement

Affects Re-sales of Units by requirement of Resale Certificates

Form 22CIC must be completed on MLS Purchase and Sale Agreements for properties that are CICs

Typically any new Plat or Condo which has 13 or more “Units/ Lots” and bills dues over $300 annually

When did the act take effect?

Effective July 1, 2018

Where does the act apply?

Washington State

Why was the act created?

To create standardization of certain aspects of CCR’s/ HOA’s/ COA’s, in connection to individual units of real estate which share Common Interest Areas.

To promote transparency in Boards and standardized access for Owners to Board meetings and information.

To Standardize Notice of Meetings of Board and to extend collections on unpaid dues to 6 years recovery.

To Provide ample information to new Buyers with Public Offering Statements and Re-Sale Certificates, with mandatory time to review before purchasing Unit.

To provide Associations with simplified remedies to revise outdated CCRs.

Questions on your transaction?

Call Ticor Title Company for clarification on how WUCIOA impacts the Title in your transaction.