Changes to the Closing Disclosure Timing

Click here to download a PDF that illustrates changes to the Closing Disclosure timeline.

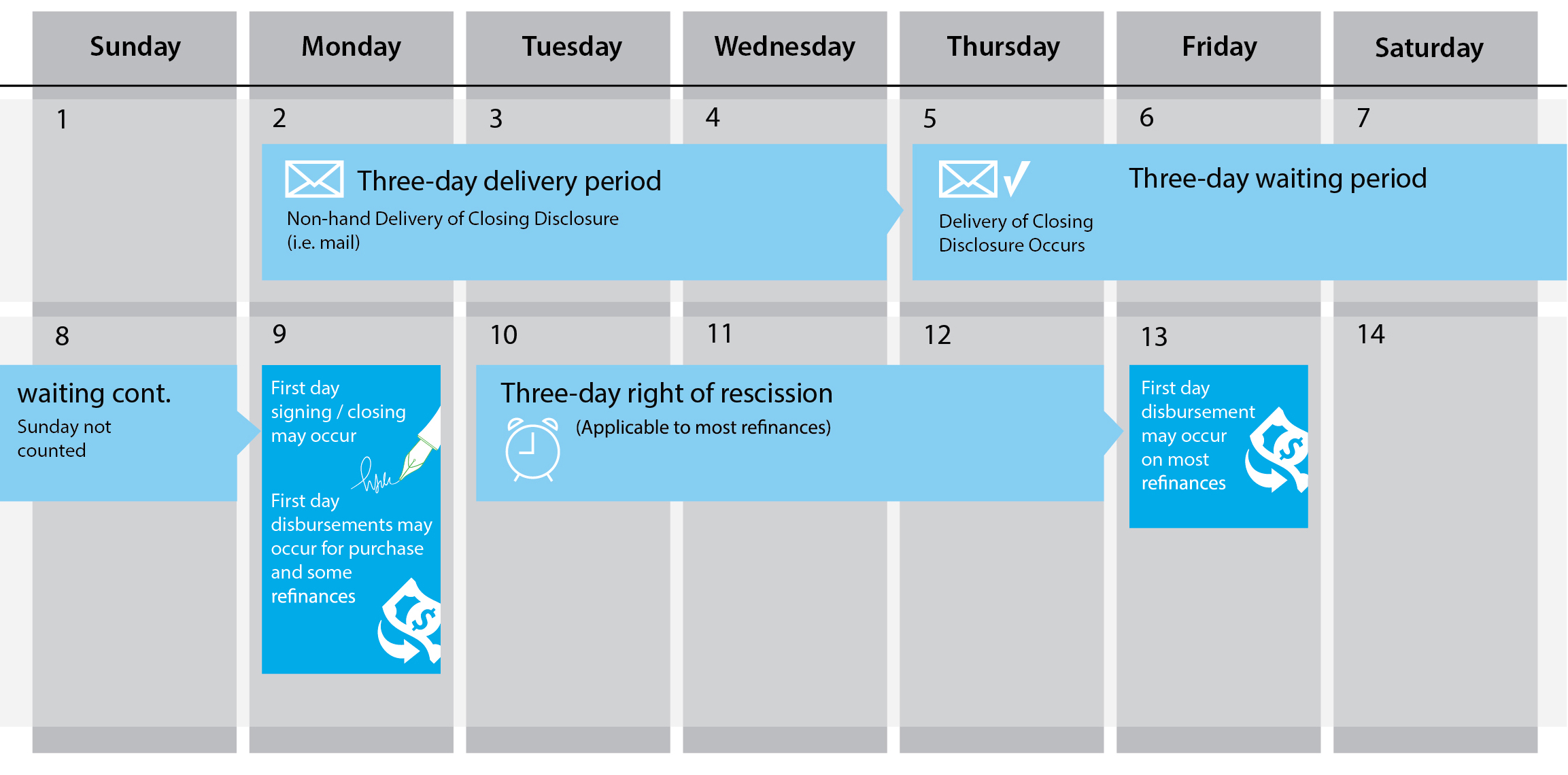

When the CFPB rules take effect in October 2015, the closing timeframes on purchases and refinances will be impacted. As part of the final rule creating the new Closing Disclosure and Loan Estimate forms, the CFPB determined that borrowers would be better served by having a short time to review the new Closing Disclosure prior to signing their loan documents. As a result, in its rule the CFPB mandated borrowers have three days after receipt of the Closing Disclosure to review the form and its contents.

However, note that the three-day review period starts upon “receipt” of the form by the borrower. Unless some positive confirmation of the receipt of the form (i.e., hand delivery), the form is “deemed received” three days after the delivery process is started (i.e. mailing). As a result, the combination of the “delivery time period” and the “review time period” results in six business days from mailing to loan signing.

Below is an illustration of how closing timeframes will be impacted

(Click the image for a larger view.)

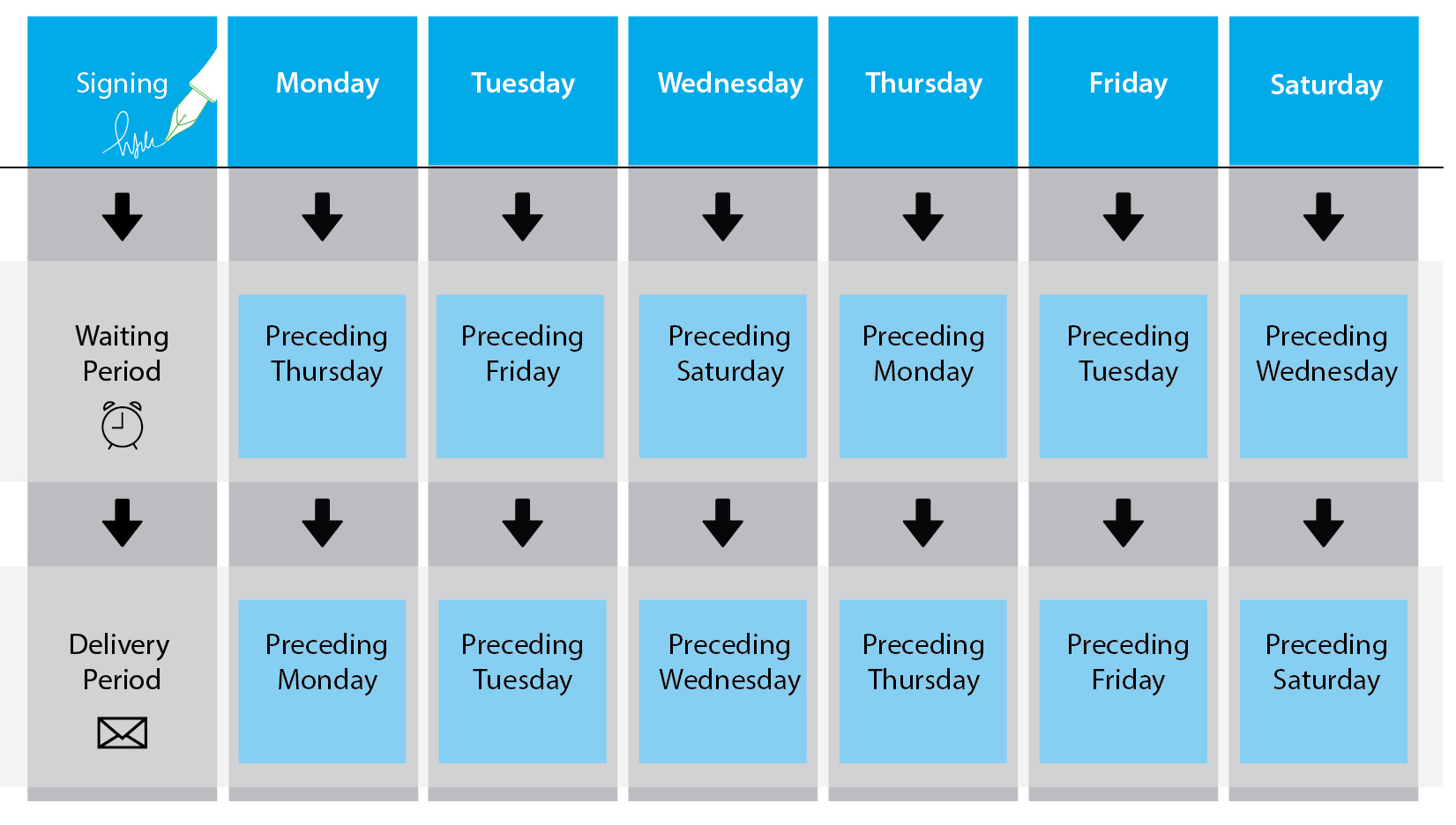

Timing references by day

(Click the image for a larger view.)

Note:

- If a federal holiday falls within the Delivery and/or Waiting Periods, add an additional business day.

- The three-day period is measured by days, not hours. Thus, disclosure must be delivered three days before closing, and not 72 hours prior to closing.

- Disclosures may also be delivered electronically to start the Delivery Period and may be signed in compliance with E-Sign requirements.