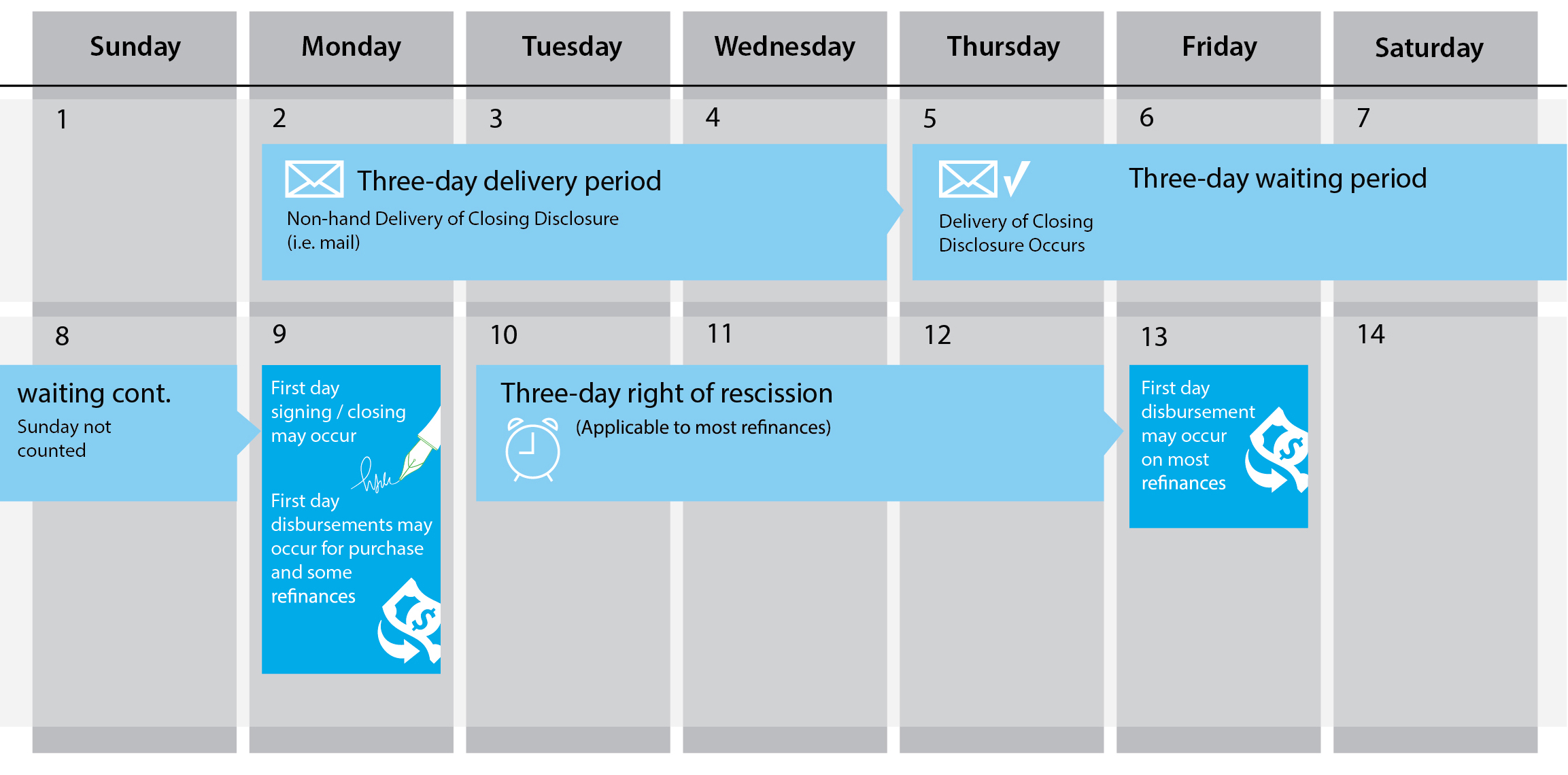

The new TRID rule has very strict requirements as to the delivery of the Closing Disclosure. The Closing Disclosure must be delivered to the borrower at least three business days prior to the consummation of the loan. If the Closing Disclosure is hand delivered, a waiting period commences which we’ll discuss further in a later post.

If the Closing Disclosure is delivered by mail, email, courier, or fax a delivery period of three business days precedes the waiting period. The delivery period does begin on the day the Closing Disclosure is sent. It does not start the next business day.

Delivery Example

If the Closing Disclosure is delivered by mail, email, courier, or fax on a Monday it is assumed the delivery period expires on Wednesday at midnight.

If the Closing Disclosure is delivered by mail, email, courier, or fax on a Monday it is assumed the delivery period expires on Wednesday at midnight.

Who Delivers the Closing Disclosure?

The rule makes the lender responsible for ensuring that the consumer receives the Closing Disclosure. Lenders may work with the settlement agent to have them deliver the Closing Disclosure to consumers on their behalf. Lenders and settlement agents also may agree to divide responsibilities with regard to completing the Closing Disclosure with the settlement agent assuming responsibility to complete some or all of the Closing Disclosure.

The lender must maintain communication with the settlement agent to ensure the Closing Disclosure and its delivery satisfy the requirements described above and the creditor is legally responsible for any errors or defects.

In the end, the CFPB will hold the lender responsible for ensuring the preparation and delivery of the Closing Disclosure is done properly regardless of who actually prepares the form and delivers it.

Wells Fargo Leads Industry

Wells Fargo led the industry by informing them of their intention to deliver the Closing Disclosure to the borrower. In September of 2014 they issued a statement which read:

Evidence of delivering the borrower’s Closing Disclosure with receipt at least three business days prior to closing are critical requirements for us. The data to support this must be readily accessible for internal and external audit. We considered many factors, such as the large number of settlement agents who close Wells Fargo loans in local markets, their closing volumes, limited integration capabilities to provide compliance data to us, and the evolving use of electronic delivery within the Wells Fargo loan process.

At this point in time, we believe that this critical compliance evidence can only be provided if Wells Fargo delivers the Closing Disclosure directly to our borrowers to meet the three-day requirement, including when a change occurs that requires the three-day clock to be restarted. We still must work closely with you to ensure we have accurate information on this disclosure, and because of the early collaboration needed, we are hopeful that this will create a smoother closing for everyone.

Transactions with a loan application made before October 3 will use the HUD-1 Settlement Statement.

Transactions with a loan application made before October 3 will use the HUD-1 Settlement Statement. Transactions with a loan application made after October 3rd will use the new Closing Disclosure Form.

Transactions with a loan application made after October 3rd will use the new Closing Disclosure Form.