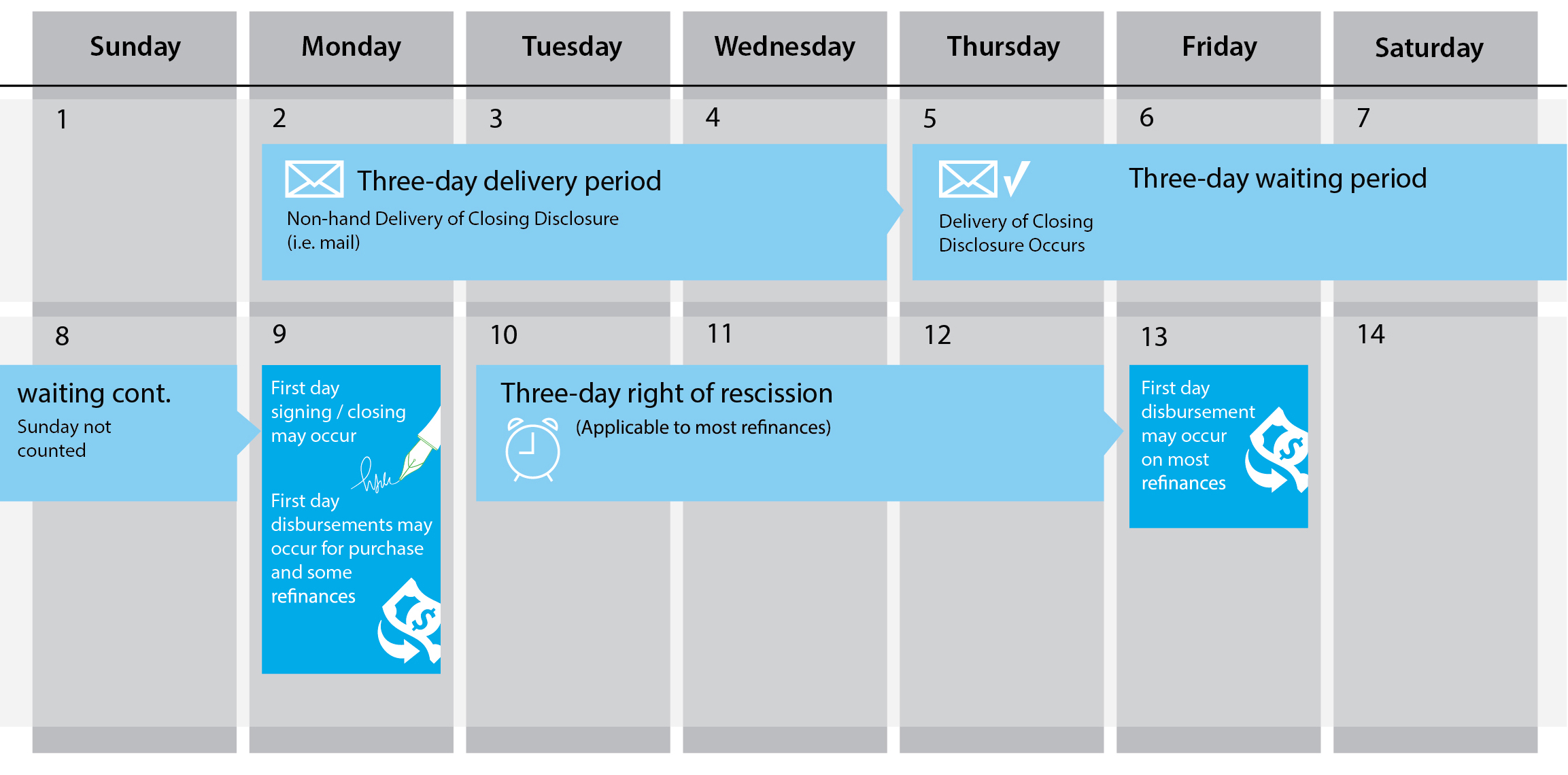

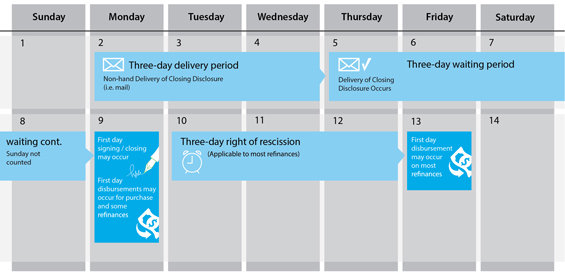

In addition to the delivery period we discussed in our previous video, lenders must ensure the borrower receives the Closing Disclosure no later than three business days before consummation. This is referred to as a waiting period.

Three Business-Day Waiting Period

The CFPB final rule requires the lender to give the borrower three business days to thoroughly review the Closing Disclosure to enable them to compare the charges to the loan estimate and ensure the cost and loan program they are obtaining are as expected. In our previous video, we explained the waiting period begins on the day the Closing Disclosure is sent. It does not start the next business day!

Waiting Period Example

If the Closing Disclosure is delivered by mail, email, courier or fax on a Monday, it is assumed that the delivery period expires on Wednesday at midnight. Then the waiting period begins, which means the loan may not be consummated less than three business days after the Closing Disclosure is received by the borrower.

The waiting period includes Thursday, Friday and Saturday, therefore the borrower would be able to sign on the next business day which is Monday, unless Monday is a federal holiday.

Exceptions to the Rule

If signing is scheduled during the waiting period, the lender must postpone signing unless closing within the waiting period is necessary to meet a bona fide personal financial emergency. Consumers may waive their right to receive the Closing Disclosure three days prior to consummation only if they have a bona fide personal financial emergency.

Bona fide personal financial emergencies are extremely rare and determining whether one exists is fact intensive. The only example provided by the CFPB is the imminent sale of the consumers’ homes through foreclosure, where the proceeds of the new mortgage can save the home from foreclosure, which isn’t very realistic.

Revisions to the Closing Disclosure

If there are changes to the loans APR, changes to the loan product, or a prepayment penalty is added to the loan after the Closing Disclosure has been delivered to the borrower, then the lender must ensure the Closing Disclosure is revised and a new delivery period and waiting period begins. For any other changes which occur before the consummation that do not include the three we just discussed, the lender must provide a corrected Closing Disclosure with any terms or cost that have changed and ensure the borrower receives it; there is no additional three business day waiting period required.

The lender must ensure only that the borrower receives the revised Closing Disclosure at or before consummation. There is no delivery or waiting period for the seller. The settlement agent must provide the seller its copy of the Closing Disclosure no later than the day of consummation.

Rescission

The rule did not make any changes to the existing rescission requirements under regulation Z. This means if the borrower is refinancing their existing loan, then the delivery, waiting, and three day right to resend applies. Keep in mind the rescission timeline is calculated differently than the delivery and waiting periods. The first day of the rescission period starts the day after all borrowers have received their notice of right to resend.