If a buyer opts not to purchase an owner’s policy, in most states they would not receive the benefit of a simultaneous issue discount applied to the loan policy premium. Currently, in a typical residential transaction, a lender quotes the discounted rate on a Loan Estimate.

However, any increase in this premium would result in a tolerance violation or increased annual percentage rate. Therefore, the CFPB wrote into the new rules any simultaneous issue discount must be applied to the owner’s policy premium and not the loan policy premium.

Therefore, when the new CFPB rules are implemented, the lender will need to disclose the full lender’s policy premium on the Loan Estimate and the preparer of the Closing Disclosure will charge the full loan premium. The new formula for calculating the owner’s premium with the simultaneous issue discount applied is as follows:

| Owner’s Premium | |

| + | Simultaneous Issue Rate |

| – | Full Loan Premium |

| = | Owner’s Rate |

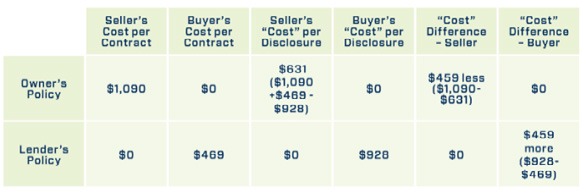

The new calculation method applies regardless of which party to the transaction is paying the owner’s policy premium. For example, the premiums on the purchase of a $300,000 residence with a $240,000 loan closed simultaneously with actual premiums are as follows:

| Owner’s Policy Premium | $1,090 |

| Loan Policy Premium (Full Rate) | $ 928 |

| Loan Policy Premium (Simultaneous Issue Rate) | $ 469 |

On a transaction closed prior to the effective date of the new rules the seller would pay $1,090 and the buyer would pay $469. On the same transaction closed after the effective date of the new rules the disclosure would reflect the seller paying the calculated premium of $631 and the buyer paying the full loan premium of $928.

The title provider will still receive all the total premium dollars due to them. However, the seller ends up paying $459 less than obligated and the buyer ends up paying $459 more than obligated.

The only way the formula works is if one of the parties to the transaction is paying both policy premiums, which in most markets is not customary. As a result, our systems have been designed to provide an off–setting debit to the seller for the balance of the owner’s premium and an offsetting credit for the same to the buyer.

The disclosure amounts, and off–setting debits and credits only appear when the Closing Disclosure is printed using the Company’s escrow production systems. Any other document, such as a closing statement or fee ticket, will print the premium dollars in the normal fashion.

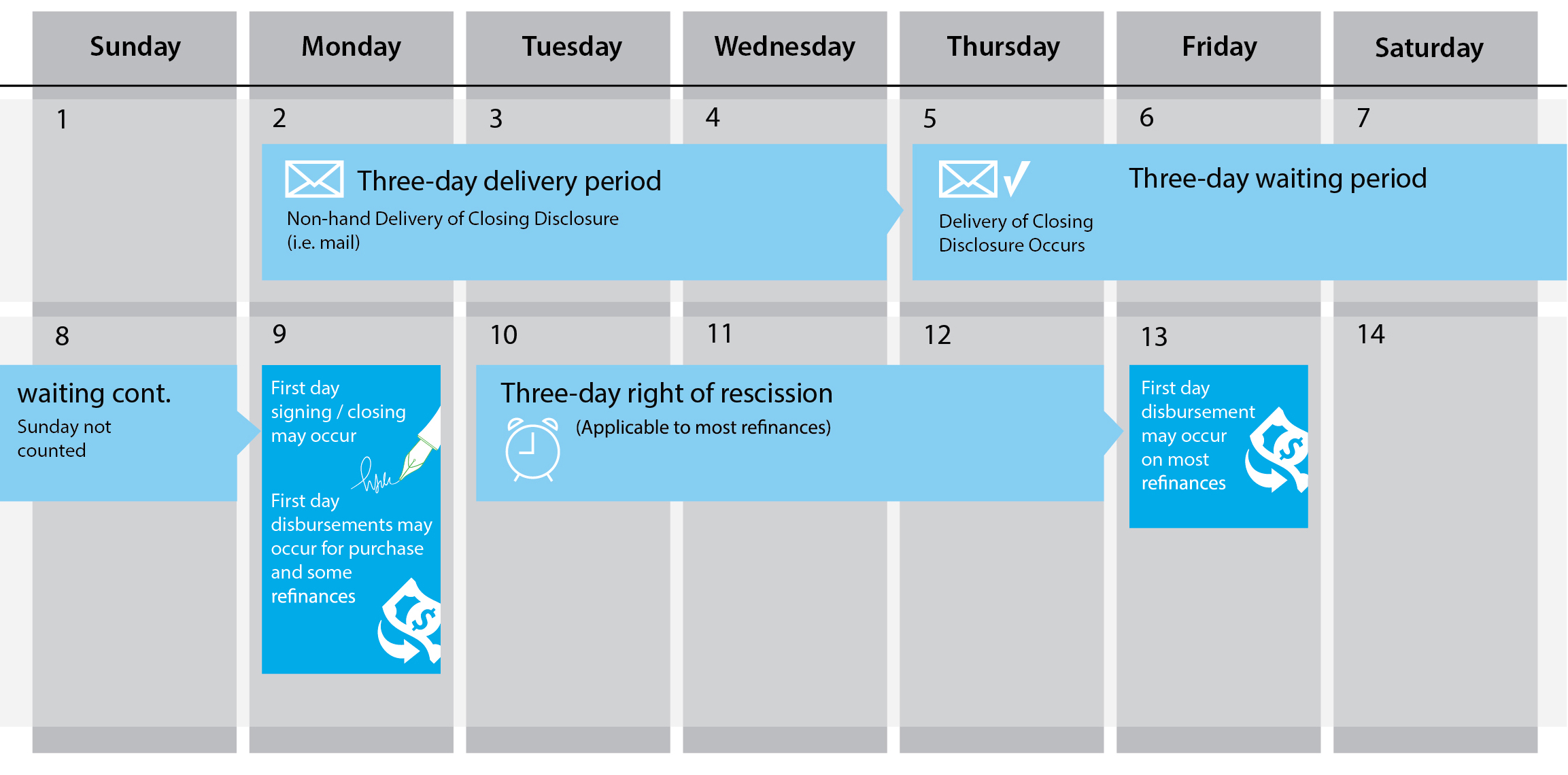

Transactions with a loan application made before October 3 will use the HUD-1 Settlement Statement.

Transactions with a loan application made before October 3 will use the HUD-1 Settlement Statement. Transactions with a loan application made after October 3rd will use the new Closing Disclosure Form.

Transactions with a loan application made after October 3rd will use the new Closing Disclosure Form.