Buying an REO (or Real Estate Owned) property involves a slightly different escrow process than your standard home sale. Realtors and Buyers need to remember that they are in escrow with a Bank/Lender (the “seller”) and the Bank/Lender has strict procedures in place that must be followed during the process. Understanding certain details can help you set the proper expectations with buyers and help ensure that your REO escrow goes as smooth as possible.

Here is a glimpse of the details to look out for if you’re in an REO transaction.

Click the image above to download tips for REO transactions.

The Seller – In an REO transaction the Seller is an “out of state” Bank. The Bank contracts a 3rd party “Asset Management Company” which represents them in the transaction and approves the final escrow closing documents. All correspondence is done by email or by their website.

Title Commitment (prelim) – Escrow will handle ordering title to insure it is ordered from the appointed “title company”. This could be a local or national division depending on the arrangements the Seller has made.

Home Owners Association (HOA) – If you are aware of an active HOA, please be sure Escrow is also notified to insure all delinquent dues are paid current at time of closing.

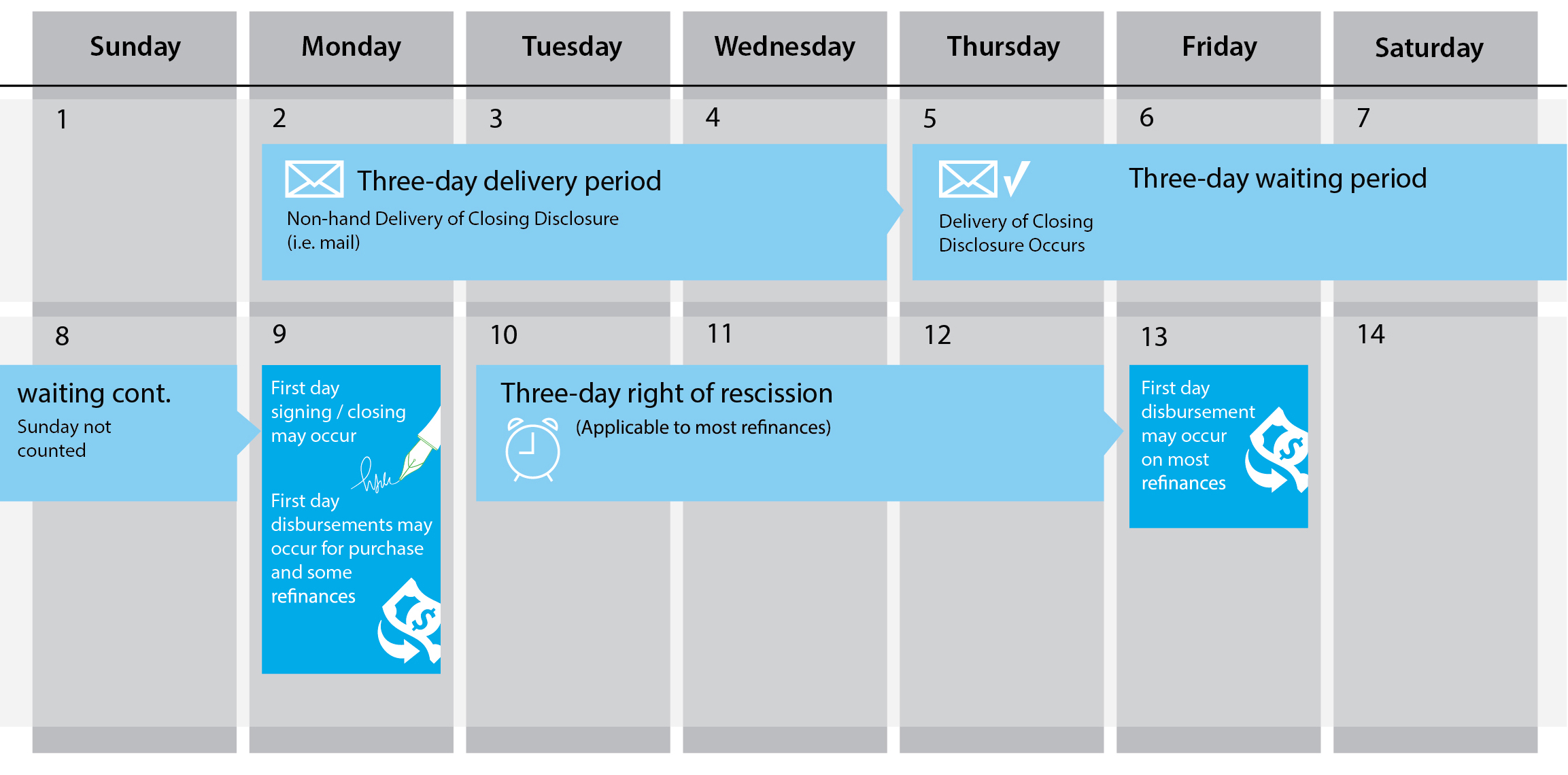

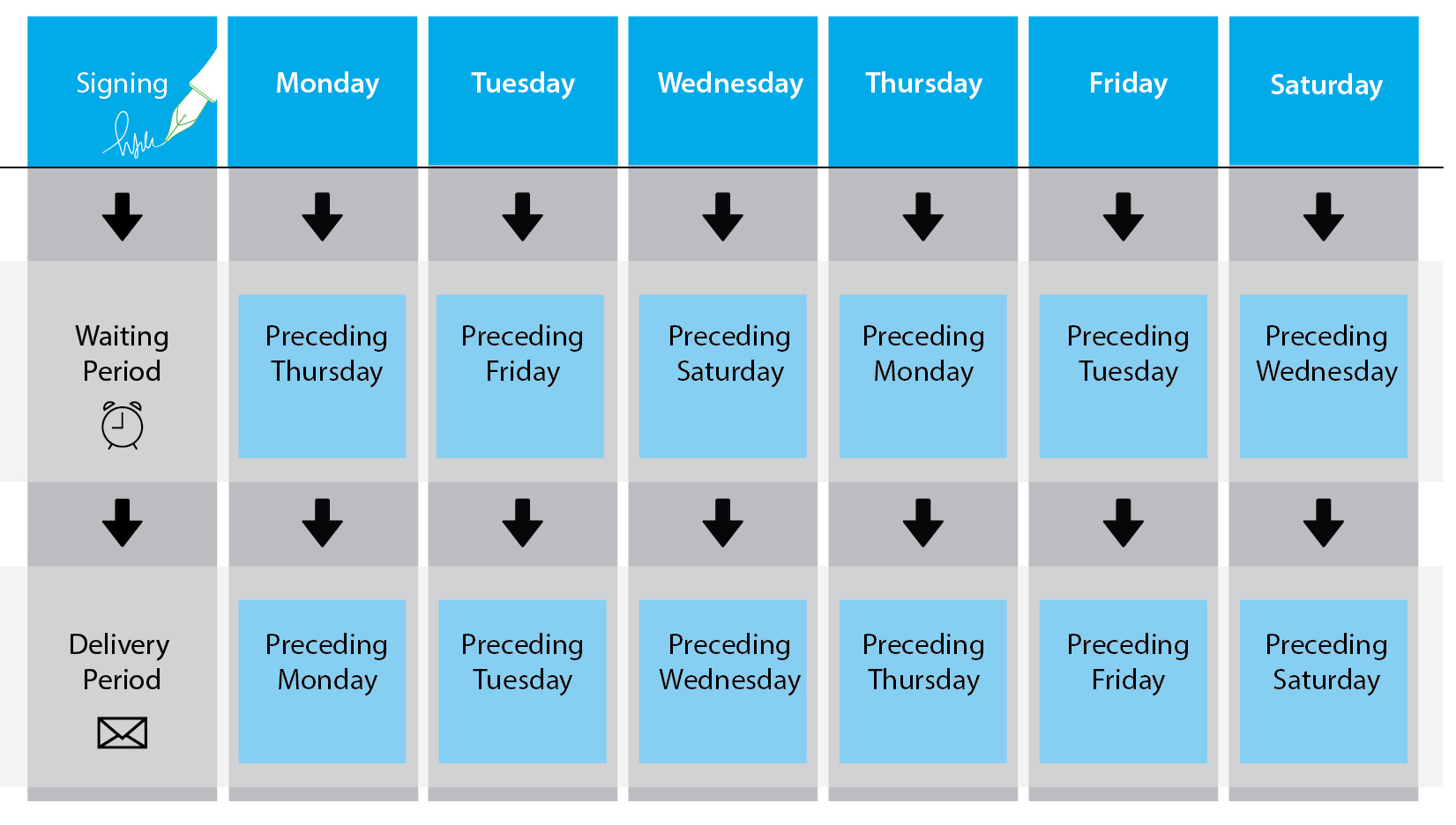

Loan Documents – Should be delivered to Escrow five working days prior to closing. Once loan documents are received and Buyer’s Lender has approved the estimated HUD Settlement Statement, escrow can set an appointment for the buyer. The earlier the documents are available, the better the chances are of an on-time closing. A HUD Settlement Statement should be available to the Lender 24 hours after receipt of Loan Documents.

Proactive Communication

Our seasoned escrow staff believes that clear, early, and frequent communication with our clients is critical with every escrow closing. With that in mind, we provide the information here to our clients immediately when an REO transaction is opened. Being aware of potential roadblocks early in the process allows time for all parties to be better prepared and sets the stage for a positive closing experience.

Courtesy Signing – If the Buyer is unable to sign with the assigned Escrow Officer, an approved Mobile Notary will be required and an additional fee could be charged. Your Escrow Officer will arrange for the courtesy signing once the loan documents have been received.

“Seller documents cannot be sent until Buyers documents have been received.”

Seller Documents – Seller documents cannot be sent until Buyers documents have been received. The REO Seller and their 3rd party Asset Company may require 24-72 hours to approve the HUD after ALL demands have been received.

Courier Fees – Buyer courier fees will be “estimated” at time of signing and adjusted to the actual cost of courier fees at the time of funding.

Buyer / Lender Funds for Closing – To meet closing deadlines, we highly recommend wiring the funds. If you send a Cashier’s Check it will need to be held in the Trust Account overnight before we can record. If a Personal Check or Official Check is presented, it could require a 10 day hold before we could close and disburse funds.

Funding – Escrow will coordinate with the Buyer’s Lender on the Bank’s HUD approval before funding can occur. (Changes to the Seller’s side of the HUD require additional Seller approval).

Have you been a part of an REO transaction where one of these potential hurdles was cleared because an escrow officer alerted you? Please share by commenting beow!