As discussed in previous videos, the lender has to disclose to the borrower services and service providers they can shop for on a provider list. The Lender is responsible for ensuring the figures stated in the Loan Estimate are made in good faith and consistent with the best information reasonably available at the time the loan estimate is issued to the borrower to ensure there are no tolerance violations. The rule tightens the tolerances and does not allow changes to even more types of charges from the Loan Estimate to the date of consummation.

Charges That Cannot Increase at Closing Now Include:

- Creditor or broker charges

- Fees charged by an affiliate of the creditor or broker

- Charges for services for which the borrower is not permitted to shop

For charges subject to zero tolerance, any amount charged beyond the amount disclosed on the loan estimate must be refunded to the borrower.

Charges With 10% Tolerance

Charges that in the aggregate cannot increase by more than 10% are:

- Recording fees

- Owners title premium

- Escrow/Closing fees

- Charges for services the consumer shopped for using the creditor’s provided list

This means the lender may charge the borrower more than the amount disclosed on the loan estimate for any of these charges so long as the total sum of the charges added together does not exceed the sum of all the charges disclosed on the Loan Estimate by more than 10%.

If the lender permits the borrower to shop for a required settlement service but the borrower either does not select a settlement service provider or chooses a settlement service provider identified by the lender on the written list of providers, then the amount charged is included in the sum of all such third party charges paid by the consumer and also is subject to the 10% cumulative tolerance. For charges subject to a 10% cumulative tolerance to the extent the total sum of the charges added together exceeds the sum of all such charges disclosed on the loan estimate by more than 10%, the difference must be refunded to the borrower.

Charges Estimated in Good Faith (Charges That May Increase)

Charges that can increase at closing, meaning they have to be estimated in good faith include:

- Prepaid interest

- Impound account setup

- Homeowner’s insurance

- Property taxes

- Charges for which the borrower chose a service provider not on the creditor’s list

- Any other non-loan related charges

If the borrower chooses a provider not on the lenders written list of providers then the lender is not limited in the amount that may be charged for the service. For certain costs or terms, lenders are permitted to charge the borrower more than the amount disclosed on the Loan Estimate without any tolerance limitation. This may include:

- Prepaid interest

- Property insurance premiums

- Amounts placed into an escrow, impound, reserve, or similar account

- Services required by the lender if the lender permits the borrower to shop and the borrower selects a third-party service provider not on the lender’s written list of service providers

- Charges paid to third-party service providers for services not required by the lenders. (May be paid to affiliates of the lender)

Lenders may only charge borrowers more than the amount disclosed when the original estimated charge or lack of an estimated charge for a particular service was based on the best information reasonably available to the lender at the time the disclosure was provided.

Tolerance Cures

The new forms group charges together making it impossible for the settlement agent to determine if there is a tolerance violation. There is no side-by-side comparison of the charges from the loan estimate to the charges shown on the closing disclosure to discern if any of them have increased.

If the amounts paid by the borrower at closing exceed the amount disclosed on the loan estimate beyond the applicable tolerance threshold, the lender must refund the excess to the borrower no later than 60 calendar days after the consummation. Although, they may cure the violation prior to consummation and it would be shown on the closing disclosure as paid outside closing to the provider covering the increased charge. The tolerance cures are shown as a lender credit on an amended closing disclosure in Section J.

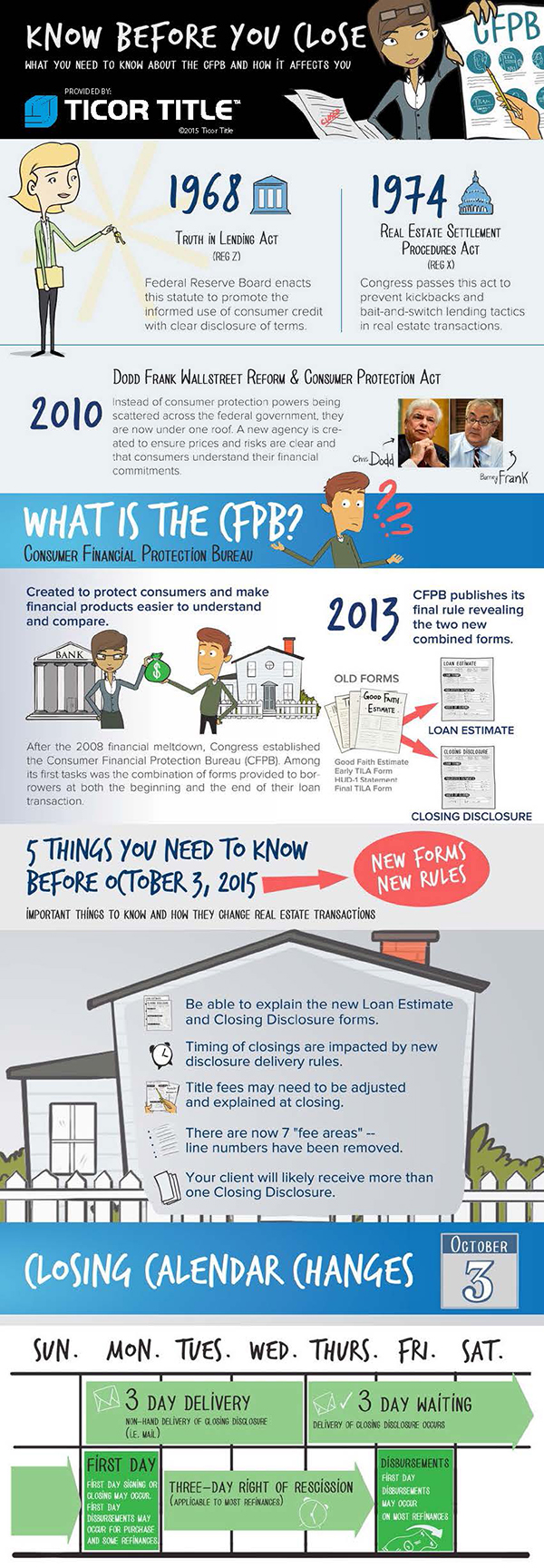

Transactions with a loan application made before October 3 will use the HUD-1 Settlement Statement.

Transactions with a loan application made before October 3 will use the HUD-1 Settlement Statement. Transactions with a loan application made after October 3rd will use the new Closing Disclosure Form.

Transactions with a loan application made after October 3rd will use the new Closing Disclosure Form.

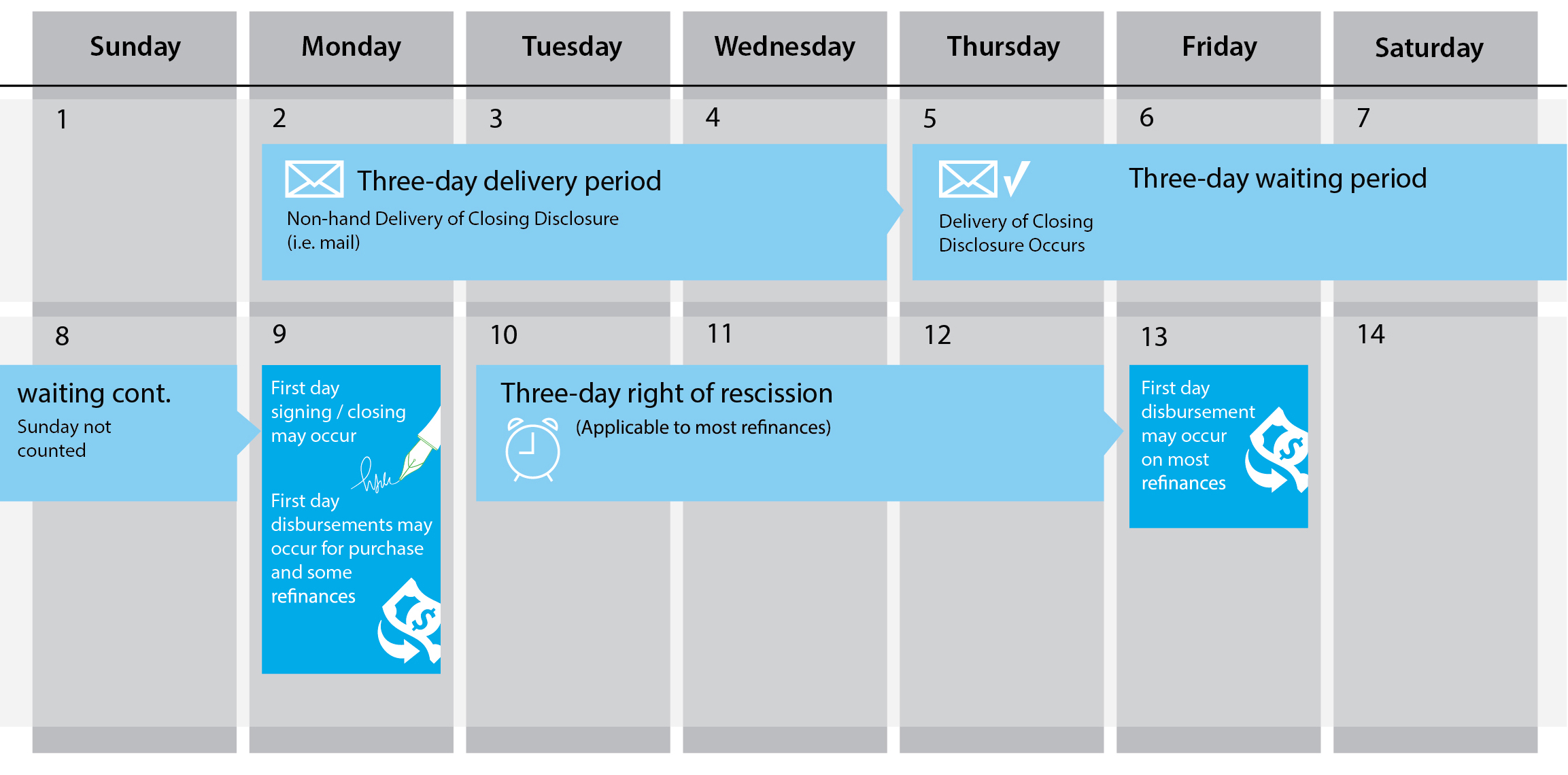

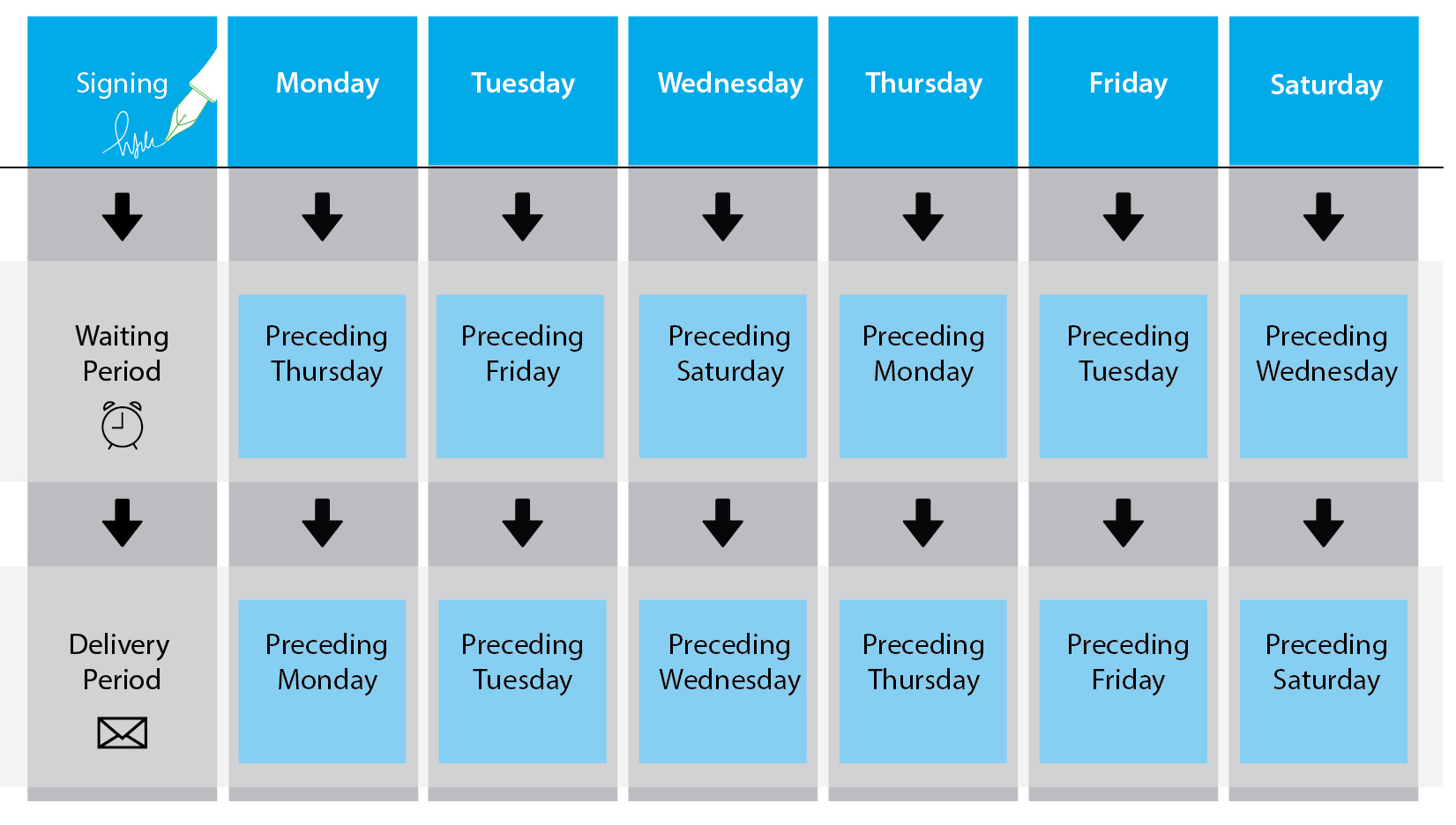

Starting October 3, 2015, the new CFPB Integrated Mortgage Disclosures under the Real Estate Settlement Procedures Act (Regulation X) and the Truth-In-Lending Act (Regulation Z) will be used for residential real estate transactions. Any residential loan originated after October 3, 2015 will be subject to the new rules and forms set forth by the CFPB. The Rule replaces the Good Faith Estimate (GFE) and early TILA form with the new Loan Estimate. It also replaces the HUD-1 Settlement Statement and final TILA form with the new Closing Disclosure.

Starting October 3, 2015, the new CFPB Integrated Mortgage Disclosures under the Real Estate Settlement Procedures Act (Regulation X) and the Truth-In-Lending Act (Regulation Z) will be used for residential real estate transactions. Any residential loan originated after October 3, 2015 will be subject to the new rules and forms set forth by the CFPB. The Rule replaces the Good Faith Estimate (GFE) and early TILA form with the new Loan Estimate. It also replaces the HUD-1 Settlement Statement and final TILA form with the new Closing Disclosure.