We are very pleased to announce that Ticor’s Gig Harbor Escrow office has relocated to an updated and more spacious location just a few doors down from the previous location.

The move is part of our plan involving the expansion of our Gig Harbor team and provides a freshly updated space with additional room to accommodate client signings, added escrow staff, and a dedicated Property Information Specialist.

We think you’ll love the upscale look & feel, accessibility, ample parking, easy access to highway 16, and our team of experienced professionals.

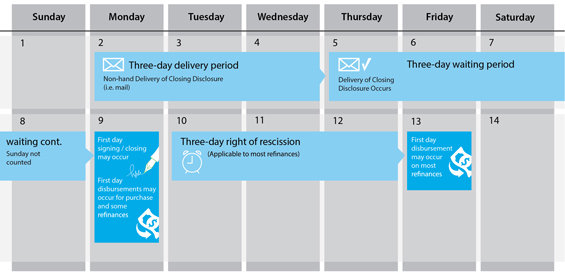

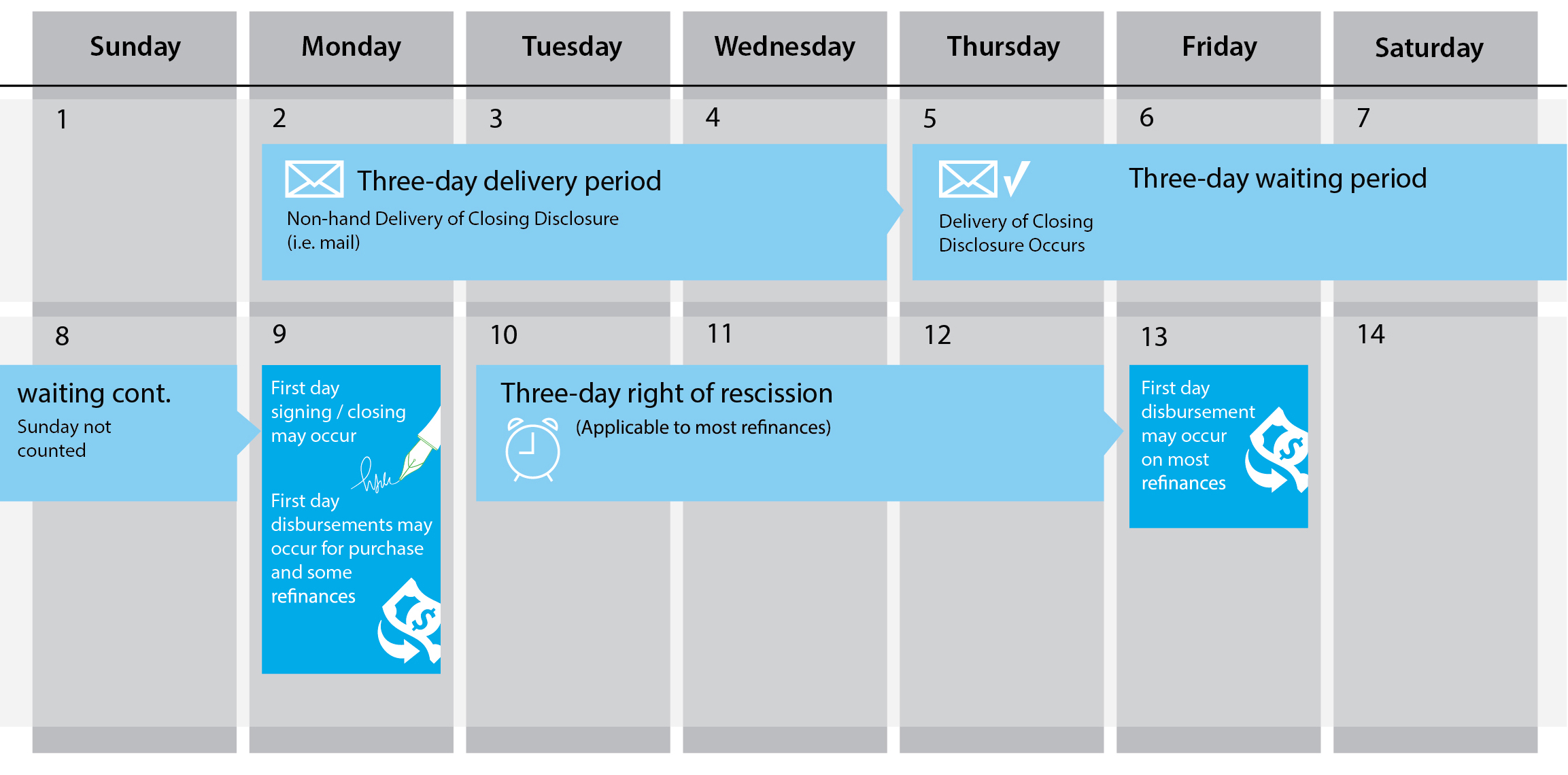

In addition to the delivery period we discussed in our previous video, lenders must ensure the borrower receives the Closing Disclosure no later than three business days before consummation. This is referred to as a waiting period.

Three Business-Day Waiting Period

The CFPB final rule requires the lender to give the borrower three business days to thoroughly review the Closing Disclosure to enable them to compare the charges to the loan estimate and ensure the cost and loan program they are obtaining are as expected. In our previous video, we explained the waiting period begins on the day the Closing Disclosure is sent. It does not start the next business day!

Waiting Period Example

If the Closing Disclosure is delivered by mail, email, courier or fax on a Monday, it is assumed that the delivery period expires on Wednesday at midnight. Then the waiting period begins, which means the loan may not be consummated less than three business days after the Closing Disclosure is received by the borrower.

The waiting period includes Thursday, Friday and Saturday, therefore the borrower would be able to sign on the next business day which is Monday, unless Monday is a federal holiday.

Exceptions to the Rule

If signing is scheduled during the waiting period, the lender must postpone signing unless closing within the waiting period is necessary to meet a bona fide personal financial emergency. Consumers may waive their right to receive the Closing Disclosure three days prior to consummation only if they have a bona fide personal financial emergency.

Bona fide personal financial emergencies are extremely rare and determining whether one exists is fact intensive. The only example provided by the CFPB is the imminent sale of the consumers’ homes through foreclosure, where the proceeds of the new mortgage can save the home from foreclosure, which isn’t very realistic.

Revisions to the Closing Disclosure

If there are changes to the loans APR, changes to the loan product, or a prepayment penalty is added to the loan after the Closing Disclosure has been delivered to the borrower, then the lender must ensure the Closing Disclosure is revised and a new delivery period and waiting period begins. For any other changes which occur before the consummation that do not include the three we just discussed, the lender must provide a corrected Closing Disclosure with any terms or cost that have changed and ensure the borrower receives it; there is no additional three business day waiting period required.

The lender must ensure only that the borrower receives the revised Closing Disclosure at or before consummation. There is no delivery or waiting period for the seller. The settlement agent must provide the seller its copy of the Closing Disclosure no later than the day of consummation.

Rescission

The rule did not make any changes to the existing rescission requirements under regulation Z. This means if the borrower is refinancing their existing loan, then the delivery, waiting, and three day right to resend applies. Keep in mind the rescission timeline is calculated differently than the delivery and waiting periods. The first day of the rescission period starts the day after all borrowers have received their notice of right to resend.

The new TRID rule has very strict requirements as to the delivery of the Closing Disclosure. The Closing Disclosure must be delivered to the borrower at least three business days prior to the consummation of the loan. If the Closing Disclosure is hand delivered, a waiting period commences which we’ll discuss further in a later post.

If the Closing Disclosure is delivered by mail, email, courier, or fax a delivery period of three business days precedes the waiting period. The delivery period does begin on the day the Closing Disclosure is sent. It does not start the next business day.

Delivery Example

If the Closing Disclosure is delivered by mail, email, courier, or fax on a Monday it is assumed the delivery period expires on Wednesday at midnight.

Who Delivers the Closing Disclosure?

The rule makes the lender responsible for ensuring that the consumer receives the Closing Disclosure. Lenders may work with the settlement agent to have them deliver the Closing Disclosure to consumers on their behalf. Lenders and settlement agents also may agree to divide responsibilities with regard to completing the Closing Disclosure with the settlement agent assuming responsibility to complete some or all of the Closing Disclosure.

The lender must maintain communication with the settlement agent to ensure the Closing Disclosure and its delivery satisfy the requirements described above and the creditor is legally responsible for any errors or defects.

In the end, the CFPB will hold the lender responsible for ensuring the preparation and delivery of the Closing Disclosure is done properly regardless of who actually prepares the form and delivers it.

Wells Fargo Leads Industry

Wells Fargo led the industry by informing them of their intention to deliver the Closing Disclosure to the borrower. In September of 2014 they issued a statement which read:

Evidence of delivering the borrower’s Closing Disclosure with receipt at least three business days prior to closing are critical requirements for us. The data to support this must be readily accessible for internal and external audit. We considered many factors, such as the large number of settlement agents who close Wells Fargo loans in local markets, their closing volumes, limited integration capabilities to provide compliance data to us, and the evolving use of electronic delivery within the Wells Fargo loan process.

At this point in time, we believe that this critical compliance evidence can only be provided if Wells Fargo delivers the Closing Disclosure directly to our borrowers to meet the three-day requirement, including when a change occurs that requires the three-day clock to be restarted. We still must work closely with you to ensure we have accurate information on this disclosure, and because of the early collaboration needed, we are hopeful that this will create a smoother closing for everyone.

This video discusses how the charge for the lenders and owners title policy must be disclosed on the loan estimate and the closing disclosure.

Where is the discount applied on the Loan Estimate and Closing Disclosure?

Traditionally, when an owner’s title policy and a loan title policy are issued at the same time, insuring the same property, a discount is applied to the cost of the loan policy. In order to prevent an increase in the loan policy premium paid by the borrower in the event where borrower elected not to purchase an optional owners policy, the CFPB requires any simultaneous issued discount be applied to the owner’s policy premium and not the loan policy premium.

How is the discount disclosed?

The rule states any title insurance policy disclosed on the loan estimate and the closing disclosure must be disclosed by adding the simultaneous issue loan premium discount for the lenders title insurance coverage to the owner’s title insurance premium and then deduct the amount of a full premium rate for the lenders title insurance policy that would be charged in the transaction when the consumer declines the purchase of an owner’s policy.

Mathematically, it all works out if the borrower is paying for both the owners and lenders title policy. Because in the end, the borrower still plays the same.

What if the Seller pays for the Owners’ Title Policy?

In areas where the seller customarily pays for the owners’ title policy, the disclosure requirements on the loan estimate and closing disclosure end up costing the buyer more than they would customarily pay. Here’s why; if the seller agreed to pay for the owners title policy and the buyer agreed to pay for the lenders title policy, but the simultaneous issue discount being offered by the title company can only be applied to the owners title policy, then the seller realizes the benefit of the discount. Keeping in mind, the discount is only offered on the lenders title policy premium.

Here’s an example:

Sale price is $180,000, the buyer is obtaining a $162,000 loan towards the purchase of the property. The purchase and sale agreement states the seller has agreed to purchase an owners title policy for the benefit of the buyer. The full premiums for each policy are: owner’s policy premium $838, lenders policy premium, at full premium rate, $727. Remember, if the policies are issued simultaneously, the lenders policy would be less; it would be $360 which represents the charge for the lenders policy premium at the simultaneous issue rate. Keeping in mind the seller is the one who agreed per the sales agreement to pay the full premium amount for the owner’s title policy.

Here’s how it would compute:

Owners’ Title Premium

$838

Simultaneous Discount Off Loan Title Policy

+

$360

Full Loan Premium

–

$727

$471

Loan title policy charge on the loan estimate and the closing disclosure is $727 paid by the borrower. Owner’s title policy charge on the closing disclosure is $471, which represents the charge for the owner’s title policy less the simultaneous discount for the loan policy. $838 for the owner’s title premium plus $360 for the simultaneous discount off the loan title policy minus $727 for the full loan premium, the total is $471 paid by the seller. This means the seller needs to give the buyer a credit for $367, which represents the difference between the charge for the owners title policy less the simultaneous discount.

Full Loan Policy Premium

$727

Simultaneous Discount Off Loan Title Policy

–

$360

$367

$727 full loan policy premium minus $360 equals $367.

In order to reconcile the charges to comply with the new rule and follow the written mutual instructions of the principles to the transaction as agreed to in the purchase and sale agreement, a debit from the borrower to the seller will have to be shown on the third page of the closing disclosure in the summaries of transactions section.

We have it covered

Don’t worry, all of the company systems are being updated, customers can still obtain accurate fee quotes which would be in compliance with the regulations using our website. Settlement agents’ production systems will be programmed to ensure the charges are disclosed properly and the purchase agreement is followed.

When the CFPB wrote the new rule, they didn’t see the need for the cost of the owner’s title policy to be disclosed on the loan estimate if the borrower is not going to pay for it. The new rule only requires the lender to disclose the cost of the owner’s title policy on the Loan Estimate if the borrower will be paying for the policy.

Unfortunately, if the borrower is paying for it, the charge must be labeled as optional on both the loan estimate and closing disclosure. This is a concern because telling a consumer owners title insurance is optional may dissuade home buyers from purchasing the same protection their lender receives. Title insurance is an insurance product like no other. And protects the homeowner for as long as they own their home.

Here are 8 more reasons why title insurance is worth the cost.

Title Insurance protects the interests of property owners and lenders against legitimate or false title claims by previous owners or lien holders. In effect it insures the investment, unlocking its potential as a financial asset for the owner.

We access, assemble, and analyze title information, in addition to handling the escrow and closing process.

Title problems are discovered in more than one-third of residential real estate transactions. These “defects” must be resolved prior to closing. The most common problems are existing liens, unpaid mortgages, and recording errors of names, addresses, or legal descriptions.

An Owner’s Title Insurance Policy protests the owner for as long as he or she has an interest in the property; and the premium is paid only once, at closing.

Title Insurance is different from other forms of insurance because it insures against events that occured before the policy is issued, as opposed to insuring against events in the future, as health, property or life insurance do. Title Insurance is loss prevention insurance.

We rely on a search of existing records to identify possible defects in order to resolve them prior to issuing a policy. We perform intensive and expensive work up-front to minimize claims. The better we do this, the lower our number of claims.

Researching titles may be extremely labor-intensive since only about 15 percent of public records are computerized. The industry invests a substantial amount of time and expense to collect and evaluate title records. As a result, the industry’s claims are low compared to other lines of insurance.

Dollar-for-dollar, Title Insurance may be the best investment a property owner can make to protect their interest.

Share the Value

The CFPB believes the consumer should make a decision to obtain Owner’s Title Insurance coverage based on available information. So talk the talk. Tell your customers about the value of Title Insurance. Share with them these eight values. Direct them to the American Land Title Association website where they can learn more about the importance of an Owner’s Title Policy.

CFPB Proposes Two-Month Extension of Know Before You Owe Mortgage Rule

October 3, 2015

On June 24, 2015, the Consumer Financial Protection Bureau (CFPB) issued a proposed amendment to the Know Before You Owe mortgage disclosure rule, which proposes to move the rule’s effective date to October 3, 2015.

“The CFPB is proposing a new effective date of Saturday, October 3. The Bureau believes that moving the effective date may benefit both industry and consumers with a smoother transition to the new rules,”

the Bureau said in the statement.

“The Bureau further believes that scheduling the effective date on a Saturday may facilitate implementation by giving industry time over the weekend to launch new systems configurations and to test systems. A Saturday launch is also consistent with existing industry plans tied to the original effective date of Saturday, August 1.”

Although the proposed effective date has changed, our commitment to help you be ready remains unchanged. We will continue to be there for you every step of the way.

As discussed in previous videos, the lender has to disclose to the borrower services and service providers they can shop for on a provider list. The Lender is responsible for ensuring the figures stated in the Loan Estimate are made in good faith and consistent with the best information reasonably available at the time the loan estimate is issued to the borrower to ensure there are no tolerance violations. The rule tightens the tolerances and does not allow changes to even more types of charges from the Loan Estimate to the date of consummation.

Charges That Cannot Increase at Closing Now Include:

Creditor or broker charges

Fees charged by an affiliate of the creditor or broker

Charges for services for which the borrower is not permitted to shop

For charges subject to zero tolerance, any amount charged beyond the amount disclosed on the loan estimate must be refunded to the borrower.

Charges With 10% Tolerance

Charges that in the aggregate cannot increase by more than 10% are:

Recording fees

Owners title premium

Escrow/Closing fees

Charges for services the consumer shopped for using the creditor’s provided list

This means the lender may charge the borrower more than the amount disclosed on the loan estimate for any of these charges so long as the total sum of the charges added together does not exceed the sum of all the charges disclosed on the Loan Estimate by more than 10%.

If the lender permits the borrower to shop for a required settlement service but the borrower either does not select a settlement service provider or chooses a settlement service provider identified by the lender on the written list of providers, then the amount charged is included in the sum of all such third party charges paid by the consumer and also is subject to the 10% cumulative tolerance. For charges subject to a 10% cumulative tolerance to the extent the total sum of the charges added together exceeds the sum of all such charges disclosed on the loan estimate by more than 10%, the difference must be refunded to the borrower.

Charges Estimated in Good Faith (Charges That May Increase)

Charges that can increase at closing, meaning they have to be estimated in good faith include:

Prepaid interest

Impound account setup

Homeowner’s insurance

Property taxes

Charges for which the borrower chose a service provider not on the creditor’s list

Any other non-loan related charges

If the borrower chooses a provider not on the lenders written list of providers then the lender is not limited in the amount that may be charged for the service. For certain costs or terms, lenders are permitted to charge the borrower more than the amount disclosed on the Loan Estimate without any tolerance limitation. This may include:

Prepaid interest

Property insurance premiums

Amounts placed into an escrow, impound, reserve, or similar account

Services required by the lender if the lender permits the borrower to shop and the borrower selects a third-party service provider not on the lender’s written list of service providers

Charges paid to third-party service providers for services not required by the lenders. (May be paid to affiliates of the lender)

Lenders may only charge borrowers more than the amount disclosed when the original estimated charge or lack of an estimated charge for a particular service was based on the best information reasonably available to the lender at the time the disclosure was provided.

Tolerance Cures

The new forms group charges together making it impossible for the settlement agent to determine if there is a tolerance violation. There is no side-by-side comparison of the charges from the loan estimate to the charges shown on the closing disclosure to discern if any of them have increased.

If the amounts paid by the borrower at closing exceed the amount disclosed on the loan estimate beyond the applicable tolerance threshold, the lender must refund the excess to the borrower no later than 60 calendar days after the consummation. Although, they may cure the violation prior to consummation and it would be shown on the closing disclosure as paid outside closing to the provider covering the increased charge. The tolerance cures are shown as a lender credit on an amended closing disclosure in Section J.

As the real estate community makes the transition to the new rules and new forms set forth by the CFPB beginning October 3, there will be a short period where pre-existing escrow transactions will close using the HUD-1 Settlement Statement and new transactions will use the new Closing Disclosure Form.

The Loan Application Date is the Determining Factor

The key factor in determining which form will be used is the date of the loan application.

In other words, transactions with loan applications made before October 3rd will use the HUD-1 Settlement Statement and transactions with a loan application date after October 3rd will use the new Closing Disclosure.

Which form will be used?

Be sure to notify us of the date of the loan application when you place your Title & Escrow order.

Loan Application Before October 3

Transactions with a loan application made before October 3 will use the HUD-1 Settlement Statement.

Loan Application After October 3

Transactions with a loan application made after October 3rd will use the new Closing Disclosure Form.

Communication is Key

Let us know the date of the loan application at the time an order is placed with us. This is the best option for a seamless, smooth transaction. If you don’t have a loan application date at the time of opening, please let us know as soon as you do so that we may ensure that the proper forms are used and your transaction is smooth and successful.

Ticor is your CFPB Readiness Partner

Regardless of the date of the Loan Application, we are prepared to serve you and dedicated to your successful transaction.

As part of the new CFPB rules, creditors are required to disclose the cost of a Title Insurance policy if it’s the borrower’s responsibility to pay for it. However, the charge must be listed as “optional” on both the Loan Estimate and Closing Disclosure, which might discourage homeowners from buying this protection.

So let’s talk about this word, “optional.” Yes, it’s technically optional, but for most people, owning a home is the biggest investment of their life! Don’t you think they should protect it? And by the way, creditors require their own title insurance policy. That’s how important they think it is to protect their investment.

Here’s something to consider: Title problems are discovered in more than a third of residential real estate transactions. Over the years, things like liens, easements, and subdivisions cause confusion over who has rights to the property, and the last thing the homeowner wants is drama that puts their investment in jeopardy. But when a consumer has an owner’s Title Insurance policy, these issues are known or resolved before signing on the dotted line, even things that are done illegally or without proper documentation giving borrowers peace of mind that their investment is protected for as long as they own the property.

So there’s our two cents about the value of an Owner’s Title Insurance Policy and listing it as an “optional” expense. The one-time cost for an owner’s title policy is a small price to pay for the peace of mind you gain. And the good news is we’re part of the nation’s largest family of title insurance underwriters, so we’ve got you covered.

To learn more about how the CFPB changes impact you, contact a local representative.

We are pleased to announce the opening of our new Title & Escrow office in Spokane. You’ll find us conveniently located at 1330 N Washington St, in the Rock Pointe Corporate Center Building. Thank you for choosing Ticor Title as your preferred Spokane Title Company!

National Strength & Local Feel

The growth of our Washington State operation has brought us into 19 counties including our newest location and dedicated staff of Title and Escrow experts serving the Spokane area. The unrivaled strength of our national brand and experience of our local professionals provide the peace of mind and personalized service levels our clients have come to expect from Ticor Title.

When you and your clients arrive at Ticor Title in Spokane, you’ll be greeted with a smile, offered refreshments, and promptly escorted to your reserved signing room. Families are welcome as we have accommodations for children as well.

We look forward to serving you at our new Spokane location and thank you for choosing Ticor Title for your residential and commercial real estate transactions.

Where to find us

Ticor Title – Spokane

1330 N Washington St.

Suite 3525

Spokane, WA 99201

Phone: 509-327-2381

Fax: 866-846-1127

Transactions with a loan application made before October 3 will use the HUD-1 Settlement Statement.

Transactions with a loan application made before October 3 will use the HUD-1 Settlement Statement. Transactions with a loan application made after October 3rd will use the new Closing Disclosure Form.

Transactions with a loan application made after October 3rd will use the new Closing Disclosure Form.