Everyone has a checklist of things they look for when buying a house, right? Like maybe looking for a quiet tree-lined street in a neighborhood with good schools not far from work. These are all important things to consider. But what about the property’s history?

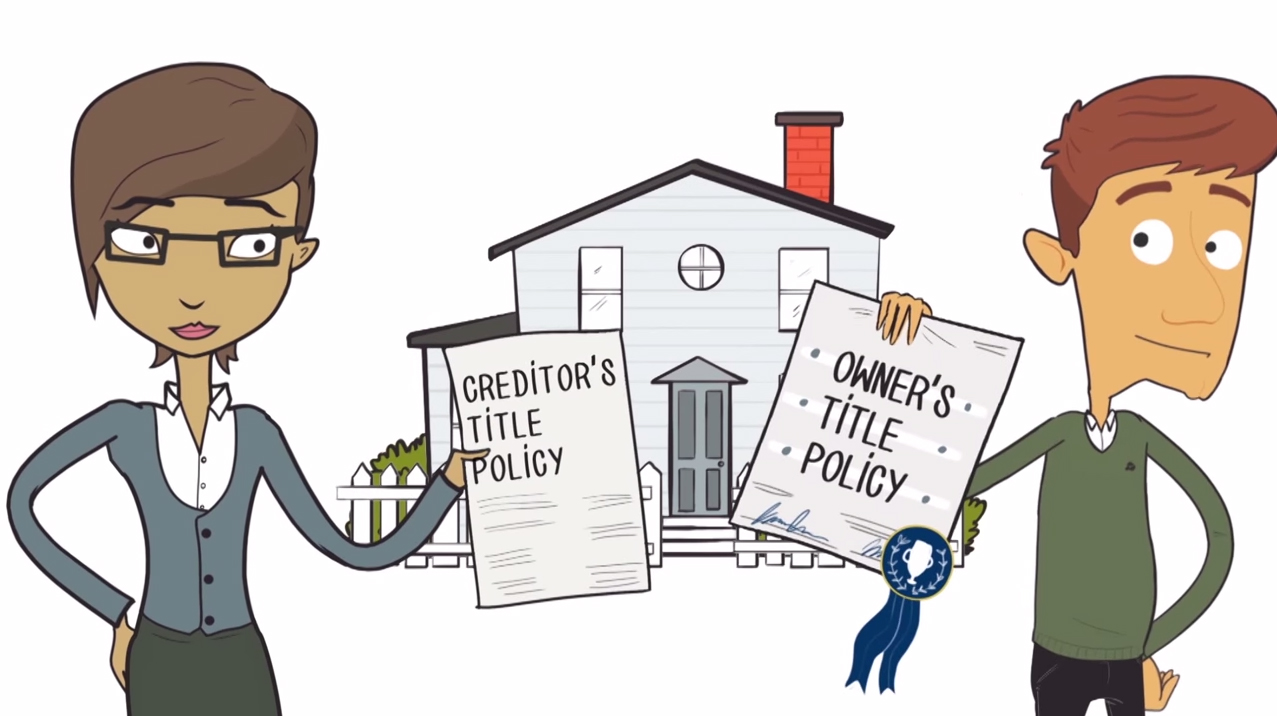

How Title Insurance Works

Over the years things like liens, easements, and subdivisions may cause confusion over who has rights to the property. And the last thing you want as a homeowner is a big kerfuffle to put your property in jeopardy! That’s where title insurance comes in. When you buy or refinance a home, title insurance confirms there are no disputes over who has rights to the property.

Related Articles

The Benefits of an Owner’s Title Insurance Policy

Water Boundaries and Title Insurance

Which Title Insurance Policy Should I Choose

Here’s how it works: Unlike auto, health, or homeowners insurance where you pay a monthly premium for value after an action, you pay for title insurance upfront to protect you from future claims.

By the time you’re ready to close the deal, title insurance gives you and your lender peace of mind that any disputes or restrictions are resolved or known. To learn more about how title insurance protects your rights to your home, contact your Ticor Title representative.

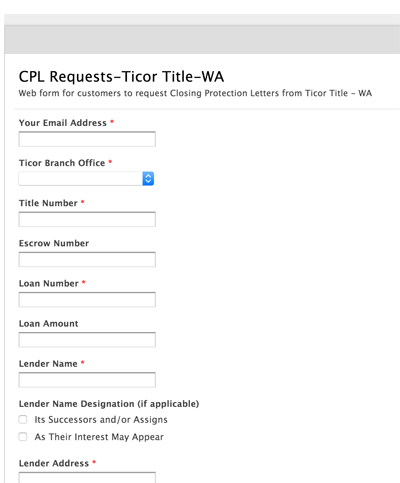

Ticor Title is proud to introduce a system by which we provide Closing Protection Letters (CPLs) in under one minute for our Lender Clients, providing convenience and a speedy response 24/7. When a Lender completes the CPL request form via MyTicor.com, a response via email with the completed CPL will be sent promptly.

Ticor Title is proud to introduce a system by which we provide Closing Protection Letters (CPLs) in under one minute for our Lender Clients, providing convenience and a speedy response 24/7. When a Lender completes the CPL request form via MyTicor.com, a response via email with the completed CPL will be sent promptly.

On December 18, President Obama signed the Protecting Americans from Tax Hikes (PATH) Act of 2015. This law creates significant changes to the provisions of the Internal Revenue Code of 1986, which amended the Foreign Investment in Real Property Tax Act of 1980 (FIRPTA).

On December 18, President Obama signed the Protecting Americans from Tax Hikes (PATH) Act of 2015. This law creates significant changes to the provisions of the Internal Revenue Code of 1986, which amended the Foreign Investment in Real Property Tax Act of 1980 (FIRPTA).

Welcome Pam Koep and Melissa Stewart!

Welcome Pam Koep and Melissa Stewart!

We are pleased to announce the opening of our new Spokane Valley Operation and that Mick Templeton AVP / Branch Manager / Escrow Closer, Melody Sarff, Escrow Assitant, and Tricia Osterholm, Escrow Assistant have joined our Spokane Ticor Team and will staff our new office.

We are pleased to announce the opening of our new Spokane Valley Operation and that Mick Templeton AVP / Branch Manager / Escrow Closer, Melody Sarff, Escrow Assitant, and Tricia Osterholm, Escrow Assistant have joined our Spokane Ticor Team and will staff our new office.