There are few things in life that are as certain as taxes, especially when it comes to buying, selling, and owning real estate. In this article, we’re going to take a specific look at common questions relating to property taxes, including when they are due, when they may be paid, how they’re calculated, and what tax relief programs are available.

Click Here to View a PDF version of this infographic.

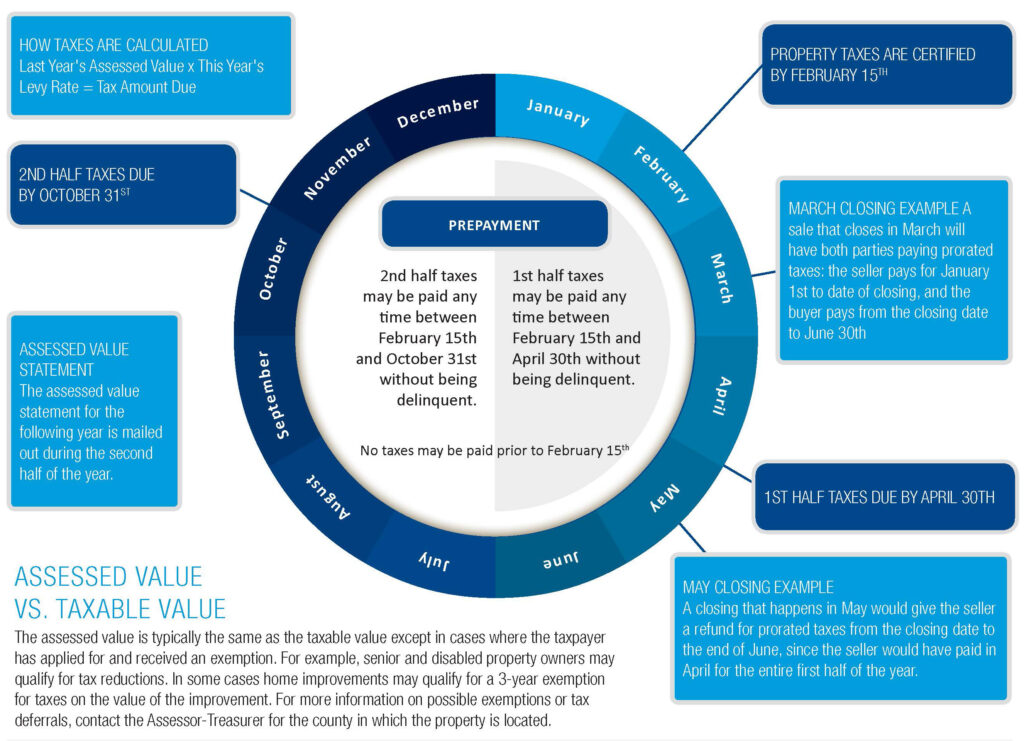

The Property Tax Timeline

Download the Property Tax infographic

Click here to download a printable version of the Property Tax annual cycle.

Property taxes have a timeline that is different than most other taxes or bills that we pay. Let’s take a look at the facts:

- Taxes are due twice a year, but towards the middle each cycle

- First half taxes are due at the end of April and cover January through June

- Second half taxes are due at the end of October, and cover July through December

Property tax proration

Because taxes are due toward the middle of the period they cover, a real estate seller may receive a refund or pay prorated taxes depending on the closing date. For example, a sale that closes in March will have both parties paying prorated taxes: the seller pays for January 1st to date of closing, and the buyer pays from the closing date to June 30th. A closing that happens in May, would give the seller a refund for prorated taxes from the closing date to the end of June, since the seller would have paid in April for the entire first half of the year.

Can property taxes be paid in advance?

When are taxes due?

1st half are due the last day of April, 2nd half are due the last day of October. King County mails out a statement in the middle of February.

Taxes for the second half of the year can be paid in advance, but the first half can’t. Washington State law (RCW 84.56.010) doesn’t allow county treasurers to collect property taxes until February 15 of the year that they are due. So the first half is typically payable any time between Feb 15th and April 30th; and the second half is typically payable any time between Feb 15th and October 31st. It is not necessary to have a tax statement to mail in with your payment. If you decide to mail in your payment without a tax statement, you must write your tax account number on the check. Mailed payments must be postmarked on or before the due date otherwise they will be considered late.

How are property taxes calculated?

How taxes are calculated

The two factors used in the calculation of taxes are the assessed value of the property and the levy rate for that area. Levy rates are represented in dollars per thousand, so to calculate the tax amount multiply the assessed value by the levy rate and divide by 1,000.

The property tax for a given parcel are based on a fairly simple calculation: multiply the total assessed or taxable value of the parcel by the levy rate for that parcel’s neighborhood. In addition there can be fees added by the county to cover specific services like noxious weed control.

Last Year’s Assessed Value x This Year’s Levy Rate = Tax Amount Due

What determines the levy rate?

The levy rates are determined by a number of factors, including the results of voter-approved levies. Property taxes usually aren’t certified until the middle of February, even though the assessments were mailed out the previous year (which often causes confusion). In other words, the assessed valuation statement you get in the 2ndhalf of this year has no effect on the taxes you are paying this year. The valuation will be used in the calculation for next year’s taxes. You won’t know the actual tax you will need to pay for 2016 until the county certifies 2016 taxes in the middle of February, even though 2016 assessed values have been available for months.

Assessed value vs. taxable value

The assessed value is typically the same as the taxable value except in cases where the taxpayer has applied for and received an exemption. For example, senior and disabled property owners may qualify for tax reductions. In some cases home improvements may qualify for a 3-year exemption for taxes on the value of the improvement. For more information on possible exemptions or tax defererals, contact the Assessor-Treasurer for the county in which the property is located.

What tax relief programs are available?

Here are some examples of tax relief programs and special classifications that may be available in your area:

- Open Space Classification for Agricultural land, Timberland, and Natural preserves.

- Designated Forest Land Classification for timberland parcels 20 acres or more.

- Historical Restoration Exemption for historical significant property undergoing restoration.

- Improvement Exemption – Single Family Dwellings a temporary exemption of valuation of additions to single-family dwellings.

- Destroyed Property Claim adjustment to the valuation of destroyed property. (King County – please note this program is handled by the Admin department, for further information please contact them at 425-388-3038).

- Property tax exemptions for senior citizens and disabled persons

- Full tax deferrals for senior citizens and disabled persons.

- Exemptions for qualifying property owned by non-profit organizations.

- Property tax deferral for those with limited income.

Property tax resources:

King County property tax resources

| King County Assessor-Treasurer hotline: | (206) 296-3850 |

| Find your tax parcel account number: | King County tax parcel search |

| See or print a tax statement: | View or print King County tax statements here. |

| Make online payment: | Pay King County Property Taxes Online |

| Make checks payable to: | King County Treasurer |

| Mailing addresses for property taxes: | King County Treasury 500 Fourth Avenue, Room 600 Seattle, WA 98104 |

Pierce County property tax resources:

| Pierce County Assessor-Treasurer hotline: | (253) 798-6111 |

| Find your tax parcel account number: | Pierce County tax parcel search |

| See or print a tax statement: | View or print Pierce County tax statements online here. |

| Make online payment: | Pay Pierce County Property Taxes Online |

| Make checks payable to: | Pierce County |

| Mailing addresses for property taxes: | Pierce County Budget & Finance P.O. Box 11621 Tacoma, WA 98411-6621 |

Snohomish County property tax resources:

| Snohomish County Assessor-Treasurer hotline: | (425) 388-3433 |

| Find your tax parcel account number: | Snohomish County Tax tax parcel search |

| See or print a tax statement: | View or Print Snohomish County tax statements online here. |

| Make online payment: | Pay Snohomish County Property Taxes Online. |

| Make checks payable to: | Snohomish County Treasurer |

| Mailing addresses for property taxes: | Snohomish County Treasurer 3000 Rockefeller Ave, M/S 501 Everett, WA 98201 |

Spokane County property tax resources:

| Spokane County Assessor-Treasurer hotline: | (509) 477-3698 |

| Find your tax parcel account number: | Spokane County Tax tax parcel search |

| See or print a tax statement: | View or Print Spokane County tax statements online here. |

| Make online payment: | Pay Spokane County Property Taxes Online. |

| Make checks payable to: | Spokane County Treasurer |

| Mailing addresses for property taxes: | Spokane County Treasurer PO Box 199 Spokane, WA 99210 |

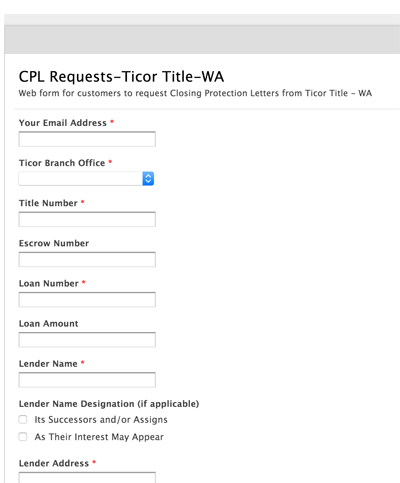

Ticor Title is proud to introduce a system by which we provide Closing Protection Letters (CPLs) in under one minute for our Lender Clients, providing convenience and a speedy response 24/7. When a Lender completes the CPL request form via MyTicor.com, a response via email with the completed CPL will be sent promptly.

Ticor Title is proud to introduce a system by which we provide Closing Protection Letters (CPLs) in under one minute for our Lender Clients, providing convenience and a speedy response 24/7. When a Lender completes the CPL request form via MyTicor.com, a response via email with the completed CPL will be sent promptly.

On December 18, President Obama signed the Protecting Americans from Tax Hikes (PATH) Act of 2015. This law creates significant changes to the provisions of the Internal Revenue Code of 1986, which amended the Foreign Investment in Real Property Tax Act of 1980 (FIRPTA).

On December 18, President Obama signed the Protecting Americans from Tax Hikes (PATH) Act of 2015. This law creates significant changes to the provisions of the Internal Revenue Code of 1986, which amended the Foreign Investment in Real Property Tax Act of 1980 (FIRPTA).

Welcome Pam Koep and Melissa Stewart!

Welcome Pam Koep and Melissa Stewart!